The Securities and Exchange Commission’s (SEC) Advisory Committee on Small and Emerging Companies met in early June to discuss various topics concerning, of course, small businesses. One of the primary topics the Committee addressed was the growing enactment and use of state-based crowdfunding (i.e. “Intrastate crowdfunding”) and how the SEC can, and should, support those efforts by modernizing Rule 147.

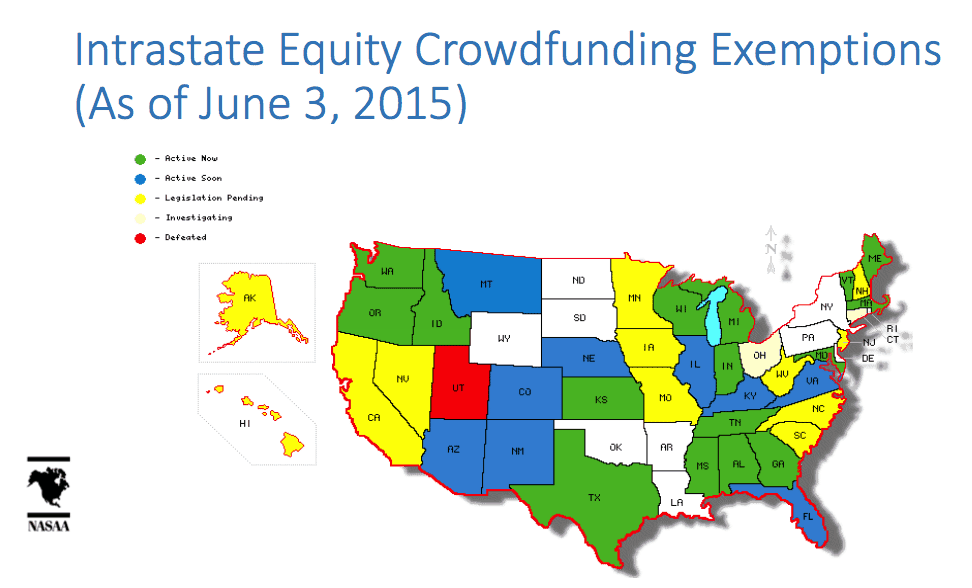

Michael Pieciak, corporate finance chair of the North American Securities Administrators Association (NASAA), lead the Committee discussions regarding intrastate crowdfunding. As he noted to the Committee “more than 16 states, including the District of Columbia, currently offer state-based crowdfunding … [and] In the very near future, we will have a majority of states having state-based crowdfunding up and running.” (for a full list of the current enacted and proposed statutes, see “STATE OF THE STATES – List of Current Active And Proposed Intrastate Crowdfunding Exemptions”). As also noted by Mr. Pieciak, one of the roadblocks to current state-based crowdfunding efforts however, is the outdated requirements of Rule 147.

Michael Pieciak, corporate finance chair of the North American Securities Administrators Association (NASAA), lead the Committee discussions regarding intrastate crowdfunding. As he noted to the Committee “more than 16 states, including the District of Columbia, currently offer state-based crowdfunding … [and] In the very near future, we will have a majority of states having state-based crowdfunding up and running.” (for a full list of the current enacted and proposed statutes, see “STATE OF THE STATES – List of Current Active And Proposed Intrastate Crowdfunding Exemptions”). As also noted by Mr. Pieciak, one of the roadblocks to current state-based crowdfunding efforts however, is the outdated requirements of Rule 147.

By way of a quick review, generally speaking INTRAstate crowdfunding means exactly that; crowdfunding that occurs solely within a single state. For example, with intrastate crowdfunding an Illinois company can raise money from Illinois residents ONLY. One of the major benefits of using any of the current intrastate crowdfunding exemptions as opposed to other options (e.g. Title II or Rule 506(c) offerings) is that the issuing company can sell the securities to both accredited and non-accredited investors (provided they live within the state of course), thus giving the issuer a much larger pool of investors to sell to. The legal basis for intrastate crowdfunding exemptions lies with Section 3(a)11 of the Securities Act of 1933 (which basically boils down to securities sold completely within a single state are exempt from federal registration). In particular, related Rule 147 (17 CFR 230.147) which creates a safe-harbor for qualifying intrastate offerings.

As Mr. Pieciak touched on in his remarks, with online based businesses and customers it has become increasingly difficult to comply with the outdated requirements of Rule 147. This led to a spirited Committee discussed regarding the challenges issuers currently face in complying with Rule 147, particularly: (i) the requirement under Rule 147 that both offers and sales be made only to residents of the companies state of formation; and (ii) the “80 percent rule” (i.e. that 80 percent of an issuer’s gross revenues be derived from operations in, assets be located in, and net proceeds of the offering be used within, the issuer’s state of operation). The primary consensus from discussion participants was that Rule 147 is outdated and needs to be modernized to reflect current business realties such as use of the internet and the regular occurrence of business transactions that cross state-borders. As SEC Chair Mary Jo White remarked with respect to Rule 147, “how an issuer might conduct an intrastate offering using the internet was not contemplated” at the time of the Rule’s adoption.

As a result of the discussions, the Committee unanimously agreed to recommend that Rule 147 be modernized. That being said, there was not a consensus from the group as to exactly how the Rule should be modernized, particularly with respect to the “80 percent rule.” As Committee co-chair Stephen Graham summed up, “[i]t makes perfect sense to modernize Rule 147 to support these state efforts … [but] We can leave it to the SEC to come up with specifics as to exactly what is doable.” The one specific recommendation that was addressed related to the requirement under Rule 147 that offers AND sales be made only to residents within the state. As David J. (DJ) Paul clarified, the Committee’s recommendation will include that Rule 147 should be revised to provide that “it is not a violation to offer [to people outside of the state], just a violation to sell [to people outside of the state].” In my opinion this is a very important point as it will help to eliminate the current illogical prohibitions against how intrastate offerings may be advertised (e.g. over the internet, through social media, etc.).

As a result of the discussions, the Committee unanimously agreed to recommend that Rule 147 be modernized. That being said, there was not a consensus from the group as to exactly how the Rule should be modernized, particularly with respect to the “80 percent rule.” As Committee co-chair Stephen Graham summed up, “[i]t makes perfect sense to modernize Rule 147 to support these state efforts … [but] We can leave it to the SEC to come up with specifics as to exactly what is doable.” The one specific recommendation that was addressed related to the requirement under Rule 147 that offers AND sales be made only to residents within the state. As David J. (DJ) Paul clarified, the Committee’s recommendation will include that Rule 147 should be revised to provide that “it is not a violation to offer [to people outside of the state], just a violation to sell [to people outside of the state].” In my opinion this is a very important point as it will help to eliminate the current illogical prohibitions against how intrastate offerings may be advertised (e.g. over the internet, through social media, etc.).

On a related note, it was brought up during the discussions that some people felt as though Title III crowdfunding, if/when enacted, would supersede the need for intrastate crowdfunding exemptions. This is actually a comment that I hear a lot from others and, in my opinion, there will still be a strong need for intrastate crowdfunding exemptions if/when Title III is enacted. First off, the offering limitations of the states are, in general, significantly higher than the current Title III cap of $1 Million. Second, even if the previous 585 pages of proposed rules governing Title III offerings is significantly reduced, it is hard to believe that they will be anywhere near as streamlined as the compliance requirements of the current intrastate crowdfunding exemptions. For these reasons, and others, I agree with the views expressed by Javier Saade, a Committee observer, who stated: “even though it seems small, [intrastate crowdfunding] will actually be quite important to the small business community in America.”

On a related note, it was brought up during the discussions that some people felt as though Title III crowdfunding, if/when enacted, would supersede the need for intrastate crowdfunding exemptions. This is actually a comment that I hear a lot from others and, in my opinion, there will still be a strong need for intrastate crowdfunding exemptions if/when Title III is enacted. First off, the offering limitations of the states are, in general, significantly higher than the current Title III cap of $1 Million. Second, even if the previous 585 pages of proposed rules governing Title III offerings is significantly reduced, it is hard to believe that they will be anywhere near as streamlined as the compliance requirements of the current intrastate crowdfunding exemptions. For these reasons, and others, I agree with the views expressed by Javier Saade, a Committee observer, who stated: “even though it seems small, [intrastate crowdfunding] will actually be quite important to the small business community in America.”

According to Mr. Pieciak, there have been only around 91 successful intrastate offerings conducted to date. As further stated by Mr. Pieciak, this “isn’t a bad start considering the majority of the rules have only been enacted for less than a year”. However, given the potential benefits to small businesses in terms of gaining access to additional capital, the question really is why are these intrastate exemptions not being used more? While part of the slow start is simply a lack of knowledge of these exemptions by issuers, a factor that is quickly becoming remedied, a larger problem is that many issuers (alone or based on the concerns of their advisers) have been reluctant to use intrastate exemptions out of fear of running afoul of Rule 147. The recommended changes to Rule 147, if enacted, will go a long way toward relieving these fears and significantly increasing the viability and use of intrastate crowdfunding exemptions.

According to Mr. Pieciak, there have been only around 91 successful intrastate offerings conducted to date. As further stated by Mr. Pieciak, this “isn’t a bad start considering the majority of the rules have only been enacted for less than a year”. However, given the potential benefits to small businesses in terms of gaining access to additional capital, the question really is why are these intrastate exemptions not being used more? While part of the slow start is simply a lack of knowledge of these exemptions by issuers, a factor that is quickly becoming remedied, a larger problem is that many issuers (alone or based on the concerns of their advisers) have been reluctant to use intrastate exemptions out of fear of running afoul of Rule 147. The recommended changes to Rule 147, if enacted, will go a long way toward relieving these fears and significantly increasing the viability and use of intrastate crowdfunding exemptions.

[scribd id=268945469 key=key-uslsqxxIOMJoqnTlPcIR mode=scroll]

Anthony Zeoli is an experienced transactional attorney with a national practice. Specializing in the areas of securities, commercial finance, real estate and general corporate law, his clients range from individuals and small privately held businesses to multi-million dollar entities. Zeoli is also an industry-recognized crowdfunding and JOBS Act expert who, most recently, has drafted a bill to allow for an intrastate crowdfunding exemption in Illinois, a copy of which can be found on his website: IllinoisCrowdfundingNow.com. Zeoli is also currently actively involved with the entrepreneurship program at the University of Illinois at Chicago as both a mentor and a student advisor and is an active advisory board member of the New York Distance Learning Association (NYDLA).

Anthony Zeoli is an experienced transactional attorney with a national practice. Specializing in the areas of securities, commercial finance, real estate and general corporate law, his clients range from individuals and small privately held businesses to multi-million dollar entities. Zeoli is also an industry-recognized crowdfunding and JOBS Act expert who, most recently, has drafted a bill to allow for an intrastate crowdfunding exemption in Illinois, a copy of which can be found on his website: IllinoisCrowdfundingNow.com. Zeoli is also currently actively involved with the entrepreneurship program at the University of Illinois at Chicago as both a mentor and a student advisor and is an active advisory board member of the New York Distance Learning Association (NYDLA).