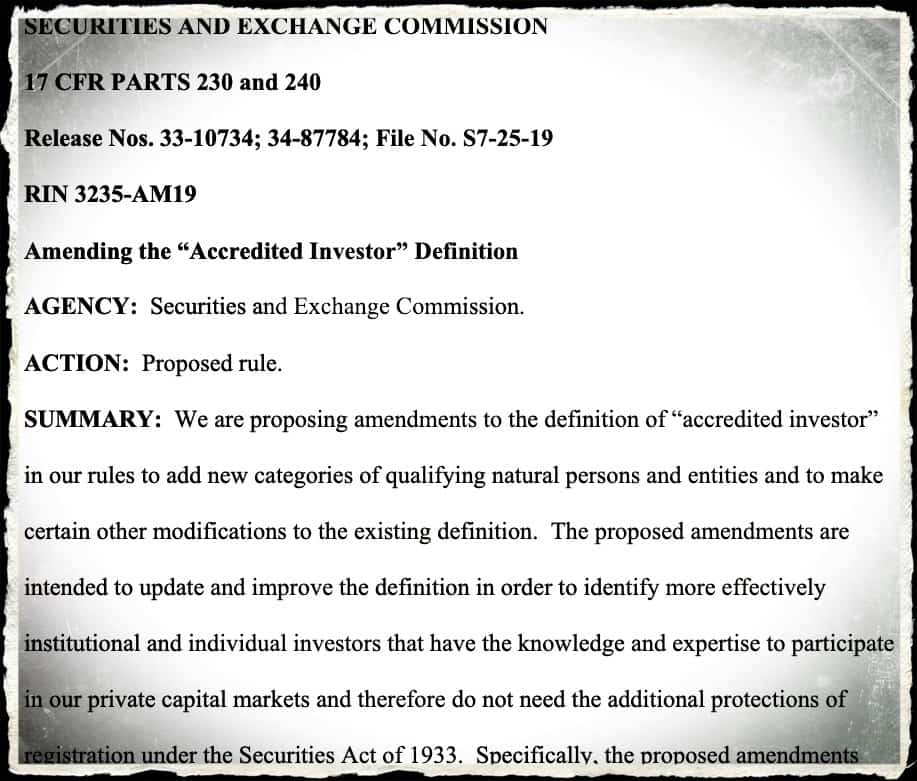

Towards the end of 2019, the Securities and Exchange Commission (SEC) proposed an update to the definition of an accredited investor. The rule change is part of a broader “concept release” that the SEC has issued to review the exempt offering ecosystem and how this can be improved.

When the rule change was revealed, SEC Chairman Jay Clayton had this to say:

“The current test for individual accredited investor status takes a binary approach to who does and does not qualify based only a person’s income or net worth. Modernization of this approach is long overdue. The proposal would add additional means for individuals to qualify to participate in our private capital markets based on established, clear measures of financial sophistication. I also am pleased that the proposal specifically recognizes that certain organizations, such as tribal governments, should not be restricted from participating in our private capital markets.”

The current definition is purely economic. If your salary is sufficient, $200,000 for an individual, or you have $ 1 million in net worth beyond your primary residence, you qualify as accredited. If you are married, your combined salary must be $300,000. The exact language is available here, if you are interested.

A blunt tool at best, just about everyone understands that the size of a bank account is not the best metric for financial acumen. Having a sophistication qualification for individuals to empower individuals to decide for themselves whether they want to invest in a private offering, simply makes more sense in the opinion of many.

Yes, there are outliers – individuals and organizations that believe there should be a heightened hurdle for investors to participate in private offerings under Reg D. But many people recognize the weakness of the argument. Any investment entails an element of risk. And younger companies tend to hold a greater degree of risk than established firms. But this is where the risk v. reward paradigm kicks in.

Investors typically are willing to shoulder more risk if the reward may be greater. A better metric would be whether or not an individual completely comprehends the intrinsic risk and the potential to lose money.

Over time, as the cost to go public has steepened dramatically, the most promising firms are seeking to remain private for as long as possible. This means the opportunity to participate in these securities offerings are shuffled off to an exclusive segment of the population – typically wealthy VC firms and individuals.

So a change of the definition is in the offing but the exact language of the final amendment is pending.

Perspectives on the current proposal differ. Some believe “it still remains policy that only rich people are permitted to get rich.”

Others view the proposal as a really big deal.

It all comes down to the final wording.

After the proposed amendment was announced, a comment period was initiated for 60 days. The deadline was Monday, March 16th. While the SEC is known for letting tardy submissions slip through, the bulk of the comments are in. So what is everyone saying?

Below is a selection of the comments from various individuals sharing their perspectives on an update to the accredited investor definition – a change that may have a significant impact on private markets.

NOTICE: Due to the Coronavirus, or COVID-19, Pandemic the Commission will not take final action on an update to the definition of an accredited investor before April 24th in order to allow commenters additional time if needed.

Maxwell R. Rich, Deputy General Counsel & Corporate Secretary, of Republic – a crowdfunding platform, shared his boots on the ground experience having dealt with many exempt offerings. Rich said:

“…in considering the types of investors that should qualify as “Accredited Investors”, we are supportive of expanding the definition to allow individuals to qualify based on measures of sophistication other than annual income and net worth.”

Rich said the operation of a securities crowdfunding platform was edifying:

“in operating our crowdfunding platform, Republic has encountered numerous examples of investors who would not meet the annual income or net worth tests which are used in place of other manners of demonstrating high levels of financial literacy and sophistication.”

Rich advocates maintaining the existing economic benchmarks but is concerned that any modification to increase these benchmarks would be highly disruptive to a very important market.

Republic’s comment letter may be viewed here.

Scott Laughlin, an Investment Analyst at CrowdStreet, a real estate crowdfunding platform, was brief in his advocacy of allowing people with sector knowledge to participate in Reg D offerings:

“I have worked at venture capital and commercial real estate funds for the past several years [as] an analyst and associate, doing the diligence and legwork behind the investments. Unfortunately, I do not meet the current standard for accredited investor, but I believe someone in my position who has been part of a fund with experience in analyzing companies and real estate deals knows the risks of investing and knows how to make wise investments. I ask that you SEC consider including an analyst level employee in the definition of “knowledgeable employee” so we can take part in investing in companies and deals we see everyday.”

Nathaniel L. Hoopes, Executive Director of the Marketplace Lending Association (MLA) – an entity that represents platforms like FundingCircle, asked the Commission to institute a sliding scale to determine investment limits for investors that do not meet the net worth or income thresholds under Rules 501(a)(5) and 506(a)(6). Additionally, Hoopes said there are better ways to define accredited investor status:

“The MLA supports amending the definition because we believe there are more accurate and inclusive ways of effectively identifying institutional and individual investors that have the knowledge and expertise to participate in the private capital markets and therefore do not need the additional protections of registration under the Securities Act of 1933 …”

Hoopes recommended that marketplace loans should not be treated as securities or limited only to accredited or institutional investors:

“We hope and encourage the Commission to propose new Crowdfunding Rules (CR) that permit the efficient and cost-effective offering of debt by lenders and thus a fully functioning retail lending marketplace similar to that of the UK crowdfunding regime. In doing so, the Commission will help more small businesses access the capital they need that the current banking system is failing to provide.”

The Marketplace Lending Association letter is available here.

Dara Albright, a long-time advocate of online capital formation and well known within the US Fintech sector, pointed to the fact that times have changed since the accredited investor rule was first minted:

“It was a very different world in 1982 when the SEC promulgated Reg D, and in doing so established the accredited investor definition. Four decades ago, the dearth of technology kept both trading commissions as well as investment minimums steep, making it impossible for small investors to self-diversify across many asset classes. Those days are long gone. Today, technology has significantly reduced the cost of financial transactions, making micro-investing a reality. Even the top discount brokerage firms have gone so far as to eliminate commission trading for conventional asset classes altogether. At the same time, technology has made it both simple and economically feasible for issuers to accommodate a sizeable number of micro-shareholders.”

Albright said that “investor-base diversification” is a topic that is rarely discussed.

“Not enough companies see the advantages in possessing a widely diverse cap table,” said Albright alluding to the fact that expanding the definition will make it more possible for issuers to have a more diverse investor base.

Albright’s comment letter is available here.

James J. Angel, a Ph.D., and Professor of Finance at Georgetown University, McDonough School of Business, slammed the current regulation as creating a “caste system” of investing that perpetuates inequality. Only the wealthiest investors benefit.

“…the SEC can now safely rely upon self-certification by investors that they meet the requirements to be accredited investors because of the increased protections of Regulation Best Interest. Selling to accredited investors does not relieve broker dealers of their Regulation Best Interest responsibilities, so the SEC can and should relax this standard. Any investor who is willing to commit securities fraud by fraudulently attesting that they meet the accredited investor standard is one who does not deserve “the protections of the Securities Act’s registration process.” Legitimately accredited investors should not be penalized with a dangerous, costly, and intrusive process because of a few liars who would only be harming themselves, if at all.”

Angel’s letter may be viewed here.

On the other side of the polemic is a group of individuals that focus more on the risk affiliated with private securities as opposed to the opportunity of investing in early-stage firms, debt, and real estate.

Barbara Roper, Director of Investor Protection, and Micah Hauptman, Financial Services Counsel, at the Consumer Federation of America (CFA), worried that expanding the definition will undermine public markets. The duo said the Commission’s “limited analysis is shockingly superficial.”

“While financial sophistication seems like a natural addition to the accredited investor definition, for decades after enactment of the ’33 Act both the SEC and courts insisted that financial sophistication alone, absent access to information, was not sufficient to satisfy the private offering exemption. In 1977, for example, the Fifth Circuit ruled on this question directly, stating that “there must be a sufficient basis of accurate information upon which the sophisticated investor must be able to exercise his skills. Just as a scientist cannot be without his specimens, so the shrewdest investor’s acuity will be blunted without specifications about the issuer.”

The CFA letter may be viewed here.

On behalf of a group of State Attorneys General, Xavier Becerra, California Attorney General, said the SEC should reject the Proposed Rule’s expansion of the accredited investor definition for individual investors for the reason that the costs of that expansion outweigh any benefits and the current wealth metric should be increased:

“Headline-grabbing businesses like Theranos and WeWork are particularly stark illustrations of the risks involved with investing in private markets. Companies that become sizeable while still private are not subject to the discipline of the public market, where corporate governance and public disclosures are meant to shed important light on companies’ operations. Without the oversight of the market—and regulators who also review public filings—companies can operate in incredibly risky ways with few consequences for negligently or even intentionally misusing investor funds.”

Xavier Becerra’s letter may be viewed here.

Lev Bagramian, Senior Securities Policy Advisor at Better Markets, Inc. – a left-leaning advocacy group, said the accredited investor definition is one of the Commission’s most important retail investor protections that should not be diluted.

“There is also little evidence showing that non-Accredited Investors actually want to invest in exempt offerings. The experience with Regulations A+ and Crowdfunding is the strongest signal that non-Accredited Investors are sending that, in fact, they do not care for exempt offerings. As detailed in the Investor Advocate’s letter, “both of these [Reg A and Reg Crowdfunding] exemptions were explicitly designed to allow companies to offer their securities to non-accredited investors…[O]f the completed offerings under Regulation Crowdfunding, the average amount raised was $208,300, well below the $577,385 maximum that was sought in the average offering.”16 Given that early-stage companies have much higher rates of failure, and the fact that non-Accredited Investors (given the dearth of their investable funds) cannot adequately diversify among high-risk firms—like venture capital and private equity investors are able to do—it is only reasonable to expect that rational non-Accredited Investors would not flock to exempt offerings.”

Bagramian’s letter may be reviewed here.