The Investor Advisory Committee (IAC) of the Securities and Exchange Commission (SEC) met yesterday to vote on the approval of its recommendations to the SEC for reforming the current definition of “accredited investor.” Most of the recommendations of the IAC call for changes to the definition which would significantly contract rather than expand the current pool of accredited investors.

In late September, the IAC released its draft recommendations to the SEC concerning potential reforms to the current definition of accredited investor. These recommendations, which consists primarily of the 4 independent suggested reforms (discussed below), were approved by the members of the IAC (with one dissenter) at its meeting yesterday. While these recommendations are only suggestive, if the SEC chooses to accept and implement any of the IAC’s constrictive recommendations, the effects on the private placement market could be disastrous.

RECOMMENDATION 1 – Potential Effect: NEUTRAL (if NO action is taken) / DECREASE NUMBER OF ACCREDITED INVESTORS.

The Commission should carefully evaluate whether the accredited investor definition, as it pertains to natural persons, is effective in identifying a class of individuals who do not need the protections afforded by the ’33 Act. If, as the Committee expects, a closer analysis reveals that a significant percentage of individuals who currently qualify as accredited investors are not in fact capable of protecting their own interests, the Commission should promptly initiate rulemaking to revise the definition to better achieve its intended goal.

The Commission should carefully evaluate whether the accredited investor definition, as it pertains to natural persons, is effective in identifying a class of individuals who do not need the protections afforded by the ’33 Act. If, as the Committee expects, a closer analysis reveals that a significant percentage of individuals who currently qualify as accredited investors are not in fact capable of protecting their own interests, the Commission should promptly initiate rulemaking to revise the definition to better achieve its intended goal.

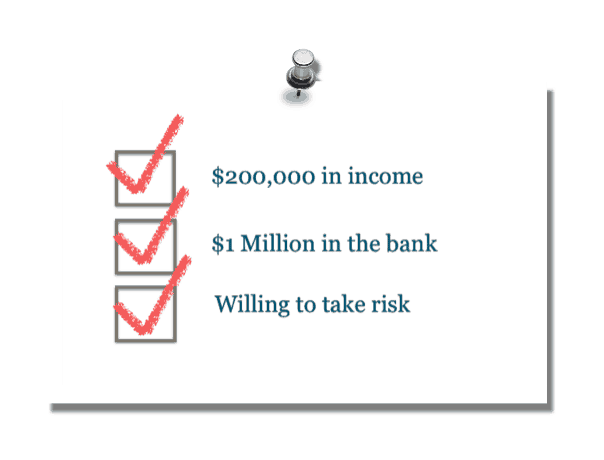

In support of the above recommendation, the IAC makes it clear that they believe the current income and net worth tests oversimplify the ability of an investor to bear the economic risks of a private investment and are not a good proxy for evaluating investor sophistication. The IAC also points out that the “income and net worth thresholds have been seriously eroded by inflation since they were first set.” These are concerns that have been raised my many people but what is most concerning is the IAC’s recommendation as to how to handle them.

The IAC makes it clear that they are not currently recommending simply adjusting the income/net worth thresholds for inflation, but they certainly leave that open as a possibility. They also suggest modifying the definition to focus on liquid assets rather than all assets and/or to potentially exclude retirement assets from the calculation. What their argument lacks however is a clear definition of why any of these suggestions are necessary.

As I read it, the IAC’s Recommendation 1 boils down to “we don’t have enough information to recommend a specific change to the current definition of accredited investor, but the current definition does not work and needs to be fixed.” Well if the IAC does not have enough information to make a recommendation, how can they say that the current definition needs to be fixed? I agree that the income/net worth tests are a poor proxy for the “3 factor” test discussed in the recommendations but the market has worked effectively for decades under the current definitions and neither the IAC nor the SEC has presented any evidence to the contrary. The 3 factor test should be used as a basis for EXPANDING the current definition not for contracting it. Any attempt to contract this definition can, and will, have a monumentally negative effect on the private placement market as discussed below. With no evidence to show why such a change is necessary, the current definition should be left as is.

RECOMMENDATION 2 – Potential Effect: INCREASE NUMBER OF ACCREDITED INVESTORS.

The Commission should revise the definition to enable individuals to qualify as accredited investors based on their financial sophistication.

The Commission should revise the definition to enable individuals to qualify as accredited investors based on their financial sophistication.

In Recommendation 2, the IAC is recommending that the definition of accredited investor be expanded to include individuals who have attained certain professional credentials and/or who have relevant professional experience without regard to their income or net worth. This recommendation was one that many of us were happy to see because it makes sense. There are several factors beyond a person’s wealth and income which could be better predictors as to whether they are sophisticated enough to make reasonable investment decisions. These include (among others) an individual’s educational background or profession.

As part of this recommendation the IAC suggests, among other things, that the definition be expanded to include individuals:

- with series 7 securities license and/or the Chartered Financial Analyst designation;

- regardless of their respective credentials, whose professional experience qualifies them as financial experts (noting, as a reference point, the U.K. test for financial sophistication, including individuals who are working, or have in the last 2 years worked, in a professional capacity in the private equity sector, or in the provision of finance for small and medium enterprises);

- based on investment experience (and an “investment owned” test); and/or

- who pass a qualification test (developed by the SEC in conjunction with FINRA, state regulators etc.)

Yes to all! This recommendation is the only one that calls for expanding the pool of accredited investors not contracting it. There are multiple potential investors who currently have the expertise and sophistication to “fend for themselves” when it comes to private investments who are shut out by the current income/net worth accredited investor tests. The U.K. has acknowledged the sophistication of similar investors and allowed them to participate in private placements and it is time the U.S. did the same. Accordingly, this recommendation should be approved and implemented by the SEC.

RECOMMENDATION 3 – Potential Effect: DECREASE NUMBER OF ACCREDITED INVESTORS.

If the Commission chooses to continue with an approach that relies exclusively or mainly on financial thresholds, the Commission should consider alternative approaches to setting such thresholds – in particular limiting investments in private offerings to a percentage of assets or income – which could better protect investors without unnecessarily shrinking the pool of accredited investors.

If the Commission chooses to continue with an approach that relies exclusively or mainly on financial thresholds, the Commission should consider alternative approaches to setting such thresholds – in particular limiting investments in private offerings to a percentage of assets or income – which could better protect investors without unnecessarily shrinking the pool of accredited investors.

Based on many of the same arguments presented in support of Recommendation 1 (e.g. imperfect proxy for evaluating investor sophistication or ability to sustain loss, etc.) the IAC recommends considering applying per investor limitations based on a percentage of such investor’s assets or income. As proposed by the IAC, these limitations would be on top of the current income/net worth tests.

[T]he Commission could retain the current income and net worth thresholds as the base value for the accredited investor definition, but restrict individuals who meet these thresholds to investing up to 10 percent of their income or net worth in private offerings in aggregate in a 12-month period.

This recommendation suffers from the same fault of reasoning as Recommendation 1 does. Neither the SEC nor the IAC has offered any evidence supporting that contention that such a limitation is necessary or that it would better protect any particular class of investors. Such a limitation however, would inevitably significantly reduce the amount of available capital in the currently private placement market. Not to mention the fact that, by the IACs recommendation above, such limitation could be included on top of changes to the overall income and net worth limitations (e.g. increases for inflation), further exacerbating the effects of any such limitation changes.

Event under the current income/net worth levels, given the potentially massive negative effect such a limitation could have on the current private placement market, to implement such a limitation would be irresponsible at best. Especially with no evidence of an upside to such limitations. Couple this with the fact that such a limitation would be extremely difficult if not impossible for issuers and crowdfunding portals to monitor and enforce, and it is clear that this recommendation should not be implemented.

RECOMMENDATION 4 – Potential Effect: UNCLEAR/ DECREASE NUMBER OF ACCREDITED INVESTORS.

The Commission should take concrete steps encourage development of an alternative means of verifying accredited investor status that shifts the burden away from issuers who may, in some cases, be poorly equipped to conduct that verification, particularly if the accredited investor definition is made more complex.

This recommendation is a little different from the others in that it does not directly deal with the accredited investor test itself but rather who should be responsible for monitoring it. In this recommendation the IAC suggests pushing the responsibility of verifying whether a person qualifies as an accredited investor to an independent third party service provider (even suggesting the function could be performed by brokers, investment advisers or an entirely unrelated verification entity). The IAC also recommends that the SEC set forth appropriate standards (e.g. with regard to accuracy, privacy and information security, etc.) for such service providers to follow in vetting investors.

I believe this recommendation has both good and bad points. Facilitating the ability of a third party verification service may help expedite the verification process as well as provide more uniform and reliable determinations. Also, the suggestion that the SEC set forth clear standards for vetting investors would be beneficial no matter who is making the decision (e.g. the issuer, a crowdfunding portal, an third party, etc.). That being said, the IAC’s reasons for wanting to push this service to a third party disturb me.

I believe this recommendation has both good and bad points. Facilitating the ability of a third party verification service may help expedite the verification process as well as provide more uniform and reliable determinations. Also, the suggestion that the SEC set forth clear standards for vetting investors would be beneficial no matter who is making the decision (e.g. the issuer, a crowdfunding portal, an third party, etc.). That being said, the IAC’s reasons for wanting to push this service to a third party disturb me.

One of the main reasons the IAC puts forth in support of this recommendation is the fact that the industry has been reluctant to make the accredited investor definition more complex because it would impose significant burdens on the verifying issuer. Put another way, if a third party verification system is used the definition could be made more complex. I have a problem with this reasoning. First, if the SEC set forth clear guidelines as recommended, I do not see why an issuer could not take on this function themselves. More importantly, I do not see a need to make the definition of accredited investor SO complex as to require an independent third party and overriding agency to vet investors.

Whether or not using a third-party service would be beneficial is unclear but I disagree with the IACs reasons for wanting to create one. If anything, I can see how under the IACs recommendation, the verification process would be made significantly more extensive and burdensome to the investor leading less investors to actually take the trouble. As a result, I believe the more likely effect of this recommendation would be to further contract the pool of accredited investors (though probably not significantly) by increasing the hoops people need to go through to be verified as accredited. Accordingly, the SEC should set forth clear verification guidelines but should not require (but could permit) the use of an independent third party verification service.

POTENTIAL IMPACT.

POTENTIAL IMPACT.

The $1 Trillion of available capital in the private placement market is the lifeblood of small-businesses and entrepreneurs and the potential impact of implementing the IAC’s recommendations could be disastrous to that market. As examined by many industry experts (including myself in a prior post “Changes To “Accredited Investor” Definition May Clip The Wings Of Many Angel Investors”), any change to the current accreditor investor test that acts to further contract the pool of potential investors could have wreak havoc with the amount of available capital currently flowing through the private placement market. Even the IAC noted in the recommendations that “simply adjusting the net worth threshold for inflation would exclude roughly 60 percent of the households that currently qualify as accredited based on net worth.” While no one knows the true effect of such a change, it is hard to imagine that effect of decreasing the available pool by 60% will be minimal.

It is clear that recommendations 1 and 3 seek to contract the currently available pool of accredited investor. The effects of these proposed recommendations are impossible to estimate but the constrictive effects could easily be equal or greater than the 60% mentioned above. It’s true that recommendation 2 seeks to expand the pool of potential investors, but I believe the potential constrictive effects of recommendations 1 and 3 will far surpass and benefit of recommendation 2. To avoid the potentially monumental economic backlash that could occur by further constricting the current pool of accredited investors, the SEC NEEDS TO IGNORE all of the IACs recommendations other than number 2.

CONCLUSION.

I can appreciate the complexity of the job the IAC and the SEC are being asked to do but I believe their priorities are out of whack. Their focus should NOT be on trying to modify the current definition as there has been no evidence supporting the proposition that it needs to be changed. In reading the IAC’s recommendations I am reminded of Jeff Goldblum’s famous line from Jurassic Park “they were so preoccupied with whether or not they could that they didn’t stop to think if they should.”

I can appreciate the complexity of the job the IAC and the SEC are being asked to do but I believe their priorities are out of whack. Their focus should NOT be on trying to modify the current definition as there has been no evidence supporting the proposition that it needs to be changed. In reading the IAC’s recommendations I am reminded of Jeff Goldblum’s famous line from Jurassic Park “they were so preoccupied with whether or not they could that they didn’t stop to think if they should.”

The private placement market currently works as it is so the current income/net worth tests should be left alone. Rather the SEC should concentrate its efforts on finding ways to include individuals who can fend for themselves as accredited investors and expanding the potential pool of capital. If not, many of the small-businesses and entrepreneurs who rely on the private capital market might become extinct.

_____________________

Anthony Zeoli is an experienced transactional attorney with a national practice. Specializing in the areas of securities, commercial finance, real estate and general corporate law, his clients range from individuals and small privately held businesses to multi-million dollar entities. Mr. Zeoli is also an industry-recognized crowdfunding and JOBS Act expert who, most recently, has drafted a bill to allow for an intrastate crowdfunding exemption in Illinois, a copy of which can be found on his website: IllinoisCrowdfundingNow.com. Anthony is also currently actively involved with the entrepreneurship program at the University of Illinois at Chicago as both a mentor and a student advisor and is an active advisory board member of the New York Distance Learning Association (NYDLA).

Anthony Zeoli is an experienced transactional attorney with a national practice. Specializing in the areas of securities, commercial finance, real estate and general corporate law, his clients range from individuals and small privately held businesses to multi-million dollar entities. Mr. Zeoli is also an industry-recognized crowdfunding and JOBS Act expert who, most recently, has drafted a bill to allow for an intrastate crowdfunding exemption in Illinois, a copy of which can be found on his website: IllinoisCrowdfundingNow.com. Anthony is also currently actively involved with the entrepreneurship program at the University of Illinois at Chicago as both a mentor and a student advisor and is an active advisory board member of the New York Distance Learning Association (NYDLA).