It could have been the kickoff of a grand political campaign – a slogan that would be proud to adorn a bumper sticker for the most ambitious of politicians – and a sound byte that would be sure to grab the next day’s headlines in the Washington, D.C. press – one that would make a Washington Democrat blush with pride. No sooner had the words been uttered, than they were greeted by resounding applause by the audience.

The words: “Millionaires can fend for themselves”.

They were spoken not by a politician running for office. Rather, this was an incumbent speaking, whose term was safe for at least another year. And his name, surely not a household word. The man: Daniel M. Gallagher, SEC Commissioner- The place – The 2014 Annual SEC Government – Small Business Forum on Small Business Capital Formation at the SEC’s Headquarters in Washington, D.C.

They were spoken not by a politician running for office. Rather, this was an incumbent speaking, whose term was safe for at least another year. And his name, surely not a household word. The man: Daniel M. Gallagher, SEC Commissioner- The place – The 2014 Annual SEC Government – Small Business Forum on Small Business Capital Formation at the SEC’s Headquarters in Washington, D.C.

But this was no bumper sticker slogan – intended to generate an immediate visceral reaction and a single message – “ vote for me.” Rather, it was a message which, when considered against a broader context, was intended to make those who heard it think – and hopefully, react.

You see, on the surface the narrow issue being addressed by Commissioner Gallagher was the wisdom of revisiting the definition of exactly who ought to be an “accredited investor”, that privileged class of investors who are empowered to invest in business ventures deemed “too risky” for the average American. Indeed, this was an issue that had not been addressed by the SEC since 1982. One of the many gems that emerged out of the Dodd-Frank Wall Street Reform and Consumer Protection Act of 2010 (Dodd-Frank) was a directive to the SEC to revisit this definition no less than once every four years. After all, weren’t “accredited investors” the real  casualties of the economic bubble that exploded in 2008, giving rise to the greatest economic calamity since the Great Depression of the 1920’s and ‘30’s?

casualties of the economic bubble that exploded in 2008, giving rise to the greatest economic calamity since the Great Depression of the 1920’s and ‘30’s?

However, what likely lies on one side of this debate are much broader issues – often articulated by Commissioner Gallagher. Could it be that what was at the root of Commissioner Gallagher’s consternation over the focus by the Commission on the definitional issue of “accredited investor” was the issue of prioritization of the Commission’s resources and, more fundamentally, the need for the Commission to regain its stride and focus. Perhaps the debate was simply ill-timed – coming at a time when a more than five year backlog of Dodd-Frank rulemaking at the SEC had broken the Commission’s back – and when the conversation needed to be directed to more pressing and neglected core missions of the SEC – enhancing capital formation and healthy secondary markets – especially for what has universally come to be viewed as the economic engine for a robust, job-creating economic recovery – small and emerging businesses.

For those who are students of Commissioner Gallagher’s many public exhortations in recent years, the message he was conveying was a simple one. Government regulation of financial markets had gone too far – and in the wrong direction. In the process the SEC has been detoured – indeed blocked – from pursuing its principal mission of promoting capital formation in U.S. markets – especially where small and emerging businesses were concerned.

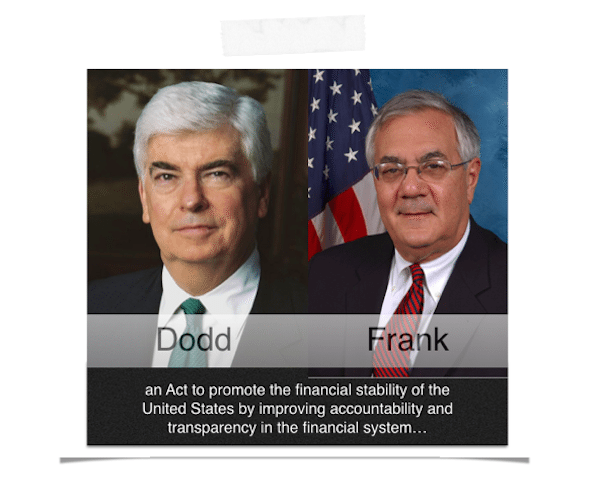

Congressman Barney Frank and his “New, New Deal” – Dodd-Frank

Had Commissioner Gallagher been given more time to address the SEC’s 2014 Annual Small Business Forum, he undoubtedly would have waxed prolific on many of the countless gifts that Congress had endowed the Commission with, neatly packaged in 2,300 pages – such as the recently enacted “Volker Rule,” the subject of years of SEC rulemaking and more than 14,000 comment letters – intended to restrict large financial institutions from trading in securities – and the “say-on-pay” rule, which remains bogged down in SEC rulemaking after receiving more than 20,000 comment letters from the public – to name but a few. Yes, the say-on-pay rule – another by-product of Dodd Frank, requiring the SEC to implement rules requiring companies to disclose the median salaries of its ordinary employees, and conspicuously disclose to investors the compensation ratio between the company’s employees and its CEO.

Had Commissioner Gallagher been given more time to address the SEC’s 2014 Annual Small Business Forum, he undoubtedly would have waxed prolific on many of the countless gifts that Congress had endowed the Commission with, neatly packaged in 2,300 pages – such as the recently enacted “Volker Rule,” the subject of years of SEC rulemaking and more than 14,000 comment letters – intended to restrict large financial institutions from trading in securities – and the “say-on-pay” rule, which remains bogged down in SEC rulemaking after receiving more than 20,000 comment letters from the public – to name but a few. Yes, the say-on-pay rule – another by-product of Dodd Frank, requiring the SEC to implement rules requiring companies to disclose the median salaries of its ordinary employees, and conspicuously disclose to investors the compensation ratio between the company’s employees and its CEO.

After all, wasn’t it those grossly overpaid CEO’s in private industry who caused the unravelling of the U.S. and world economy in 2008. And surely, by requiring the SEC to mandate disclosure of these inequities couldn’t one expect the U.S. and world economy to right-size itself – by redistributing compensation in a more equitable fashion. And if nothing else, this newly disclosed data would give testament to those who believe that it was capitalism itself that had caused the American Dream to go awry. And the fix: more government and regulatory oversight of private enterprise.

And in case the Volker Rule and say-on-pay would not be enough to stabilize the U.S. economy, perhaps one or more of the dozens of additional rules which the SEC was charged with promulgating would do the trick.

But what about those millions of American jobs that vanished overnight in 2008 and 2009, drawing historic comparisons to the bread lines of the Great Depression? How was Dodd-Frank going to solve that problem? Well, Barney Frank was way ahead of all of us – simply package Dodd-Frank as the “new, new deal” and add “consumer protection” to the name of the bill following his moniker. Though this did little to assuage the concerns of his fellow Republicans in the House of Representatives, all of whom voted against Dodd-Frank, this legislation sailed through a Democratic Congress and White House in record time – within months of President Obama’s historic inauguration.

Seems that Congressman Barney Frank was more a student of politics and rhetoric than the history of the Great Depression – and the time tested wisdom of FDR’s New Deal. Though like Dodd-Frank, the Securities Act of 1933 also sailed through Congress during the first few months of FDR’s administration as part of his New Deal, with legislation creating a comprehensive regulatory scheme for financial markets, followed by the Securities Exchange Act of 1934, and the creation of the Securities and Exchange Commission, this is where the comparison with Dodd-Frank both begins and ends.

Seems that Congressman Barney Frank was more a student of politics and rhetoric than the history of the Great Depression – and the time tested wisdom of FDR’s New Deal. Though like Dodd-Frank, the Securities Act of 1933 also sailed through Congress during the first few months of FDR’s administration as part of his New Deal, with legislation creating a comprehensive regulatory scheme for financial markets, followed by the Securities Exchange Act of 1934, and the creation of the Securities and Exchange Commission, this is where the comparison with Dodd-Frank both begins and ends.

Perhaps the Barney Franks of the world could use a history lesson as to what FDR’s New Deal looked like, when this country was faced with The Great Depression and historic levels of unemployment which followed in its wake.

A Lesson in History

Like his counterpart Barack Obama, FDR surely was the epitome of a Democratic liberal, not one of those conservatives who had steered this country off course leading up to the economic calamities which surfaced in 2008. FDR summed up his political leanings best in this quote:

“A conservative is a man with two perfectly good legs, who, however, has never learned to walk…. A liberal is a man who uses his legs and his hands at the behest of his head.”

But this is where FDR’s New Deal, and the raw deal of Dodd-Frank, part company.

But this is where FDR’s New Deal, and the raw deal of Dodd-Frank, part company.

The excesses of the 1920’s which culminated in the 1929 Stock Market Crash and the economic depression which succeeded it have been well documented. The financial markets where securities traded were only loosely regulated, with insiders dominating what essentially was in many respects a rigged and unsavory market. Insider trading was the order of the day, with unrestricted short selling and market manipulation, replete with “wash sales” etc. And many an average American was lured from the more protective New York Stock Exchange with promises of easy riches to unregulated “curb exchanges”, where shares changed hands, literally on the sidewalk, free of Big Board listing rules.

Indeed, it seemed as though the U.S. securities markets in the 1920’s were for many average Americans the hope, the path, to achieving the American Dream. “Everyone ought to be rich,” pronounced a Ladies Home Journal article published in the heyday of the 1920’s. In hindsight, the lure of the American dream proved to be illusory, indeed disastrous, for many Americans, So too did the unbridled lending practices facilitated by the government regulated Fannie Mae and Freddie Mac since the late 1990’s – under the not so watchful eye of Congress – in what in hindsight was the perfect political storm: the promise of homes for all Americans – with government backed financing – and handsome, seemingly endless profits for Wall Street through the resale of bundled mortgages to an unsuspecting market with a seemingly voracious appetite.

In hindsight, the intersection of Main Street and Wall Street in the 1920’s, fueled by greed, the American Dream and poorly regulated financial markets, proved to be the undoing of the American Dream – indeed, the scene of an economic wreck.

Out of the debacle of the 1920’s came both a new President, and a “New Deal”, intended to both rekindle confidence in this country’s capital markets and to move Americans from the bread lines to full time gainful employment. Likewise, Dodd-Frank was intended to rekindle confidence in America’s financial markets. But to what end for the average American?

Out of the debacle of the 1920’s came both a new President, and a “New Deal”, intended to both rekindle confidence in this country’s capital markets and to move Americans from the bread lines to full time gainful employment. Likewise, Dodd-Frank was intended to rekindle confidence in America’s financial markets. But to what end for the average American?

An important piece of the New Deal legislation was the Securities Act of 1933, regulating sales of securities by issuers, and the Securities Exchange Act of 1934. And unlike Dodd-Frank, which was rushed through a politicized Congress in a matter of months before Congressional hearings took place, to identify the real causes of the 21st Century global economic meltdown, the regulatory reforms embedded in these two historic post-1929 pieces of legislation were the result of careful study and a multitude of Congressional hearings spanning over a period of years. According to one historical account, early New Deal legislation “was an attempt by FDR at compromise – an effort to get both private enterprise and the federal government working together to create a stronger, more equitable economy.”

And to administer this new regulatory regime the U.S. Securities and Exchange Commission was created, with an initial reported budget of $300,000 and offices shared with the Federal Trade Commission. Indeed the FTC was the agency initially charged with overseeing this new regulatory scheme – at least until FDR decided that it would be much wiser, and more efficient, to have an agency with a single, focused purpose to regulate U.S. capital markets.

And to administer this new regulatory regime the U.S. Securities and Exchange Commission was created, with an initial reported budget of $300,000 and offices shared with the Federal Trade Commission. Indeed the FTC was the agency initially charged with overseeing this new regulatory scheme – at least until FDR decided that it would be much wiser, and more efficient, to have an agency with a single, focused purpose to regulate U.S. capital markets.

Placed in charge of this enormous undertaking by FDR as the SEC’s first Chair was Joseph P. Kennedy, who by his own admission reaped enormous profits in the 1920’s from trading on inside information, short sales and market manipulation – all perfectly legal at the time. He was also one who knew a bubble when he saw one – selling his positions and placing his capital into safer government securities before the markets came crashing down.

History records that shortly following the enactment of the Securities Exchange Act of 1934, the sluggish capital markets, distrusted by small investors and big business alike, had come back to life.

The Obama White House’s Global Entrepreneurial Summit – America’s Answer to the Great Recession?

Meanwhile, back in 2010 it seems that the average American worker (or would be worker) fared no better at the White House than it did with Dodd-Frank in the halls of a Democratically controlled Congress. Though the rhetoric of President Barack Obama emanating from the White House was hopeful, like Dodd-Frank it was focused on the wrong place – and at the wrong time. Indeed, it seemed as though while Rome was burning – Nero was fiddling – with the wrong tune.

Meanwhile, back in 2010 it seems that the average American worker (or would be worker) fared no better at the White House than it did with Dodd-Frank in the halls of a Democratically controlled Congress. Though the rhetoric of President Barack Obama emanating from the White House was hopeful, like Dodd-Frank it was focused on the wrong place – and at the wrong time. Indeed, it seemed as though while Rome was burning – Nero was fiddling – with the wrong tune.

It was April 2010, where President Obama proudly presided over the inaugural Global Entrepreneurship Summit at The White House – something he considered one of his first signature accomplishments of his nascent presidency. Surely our President would understand the need to re-grow our sagging economy “from the bottom up,” expanding the opportunity of the average American to receive a paycheck instead of a handout – and pursue the American Dream. Indeed, his words were inspirational:

“We’re forging new partnerships in which high-tech leaders from Silicon Valley will share their expertise — in venture capital, mentorship, and technology incubators . . . .

And tonight, I can report that the Global Technology and Innovation Fund that I announced . . . will potentially mobilize more than $2 billion in investments. This is private capital, and it will unlock new opportunities for people . . . in sectors like telecommunications, health care, education, and infrastructure.

And finally, I’m proud that we’re creating here at this summit not only these programs that I’ve just mentioned, but it’s not going to stop here. Together, we’ve sparked a new era of entrepreneurship — with events all over Washington this week, and upcoming regional conferences . . .”

And as to the rhetorical question posed by the President: “why a summit on entrepreneurship? “ In his words: “The answer is simple”.

And as to the rhetorical question posed by the President: “why a summit on entrepreneurship? “ In his words: “The answer is simple”.

“Entrepreneurship — because you told us that this was an area where we can learn from each other; where America can share our experience as a society that empowers the inventor and the innovator; where men and women can take a chance on a dream — taking an idea that starts around a kitchen table or in a garage, and turning it into a new business and even new industries that can change the world.”

“Entrepreneurship — because throughout history, the market has been the most powerful force the world has ever known for creating opportunity and lifting people out of poverty.”

“And social entrepreneurship — because, as I learned as a community organizer in Chicago, real change comes from the bottom up, from the grassroots, starting with the dreams and passions of single individuals serving their communities.”

Leaving no doubt that this intense focus on entrepreneurship borne back in the spring of 2010 was an overwhelming success, The White House had this to say on the eve of the fifth World Entrepreneurship Summit in November 2014:

“President Obama elevated entrepreneurship to the forefront of the United States’ engagement agenda . . .. The Administration has delivered on this commitment, greatly expanding support for entrepreneurship and economic opportunity . . .. Signature achievements in the past five years include:

“The Administration has committed roughly $3.2 billion to support micro, small, and medium sized enterprises and mobilized $80 million in private capital for startup accelerators . . . .”

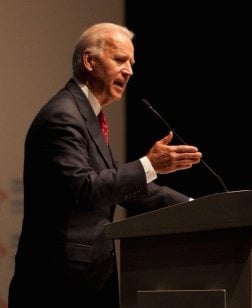

And to showcase the importance of the Fifth Entrepreneurial Summit, attended by nearly 4,000 people, was a slew of U.S. dignitaries, including Vice President Joe Biden, SBA Administrator Maria Contreras-Sweet and a host of cabinet members, senior U.S. Government officials and other heads of U.S. agencies – paid for by “ours truly” – the American taxpayer.

And to showcase the importance of the Fifth Entrepreneurial Summit, attended by nearly 4,000 people, was a slew of U.S. dignitaries, including Vice President Joe Biden, SBA Administrator Maria Contreras-Sweet and a host of cabinet members, senior U.S. Government officials and other heads of U.S. agencies – paid for by “ours truly” – the American taxpayer.

Vice President Biden’s words to the audience captured the importance of the entrepreneurial undertakings:

“The single most valuable resource on this planet I think we could all agree on in this room is not what’s in the ground, but what’s in the mind. It’s the single least explored part of the world, the mind. The things that are going to happen in the next two, five, 10, 15 years are breathtaking. Investors, they have to be willing to expand the horizon and invest in early stage entrepreneurs — not only in Silicon Valley — but . . . everywhere, everywhere where there’s talent.”

“Governments have to unlock the marketplace of ideas by allowing people to express their views openly about what they’re thinking and what they’re trying.”

“They must unlock the commercial marketplace by eliminating barriers to access to capital; ensuring that rules are fair and predictable, removing excessive cumbersome regulations.”

“The government can’t grow the economy by itself. As a matter of fact, it’s not the major reason. It’s a catalyst for growth — no matter how big the megaproject. To prosper in the 21st century, you also need to grow from the bottom up, allowing your people to unlock their talents through private enterprise and political and economic freedom and action”

Sadly, however, neither our President nor our Vice-President was addressing the American Dream – rather, they were addressing another dream: to export American entrepreneurialism, and capital, to countries around the World. However noble these aspirations may have been, they were focused on the wrong place – and at the wrong time.

Sadly, however, neither our President nor our Vice-President was addressing the American Dream – rather, they were addressing another dream: to export American entrepreneurialism, and capital, to countries around the World. However noble these aspirations may have been, they were focused on the wrong place – and at the wrong time.

And four and one half years later, at practically the same moment that Vice President Biden was addressing the Fifth Global Entrepreneurial Summit, in Marakech, Morocco, Commissioner Gallagher made his plea for economic and regulatory sanity at the SEC’s 2014 Annual Small Business Forum, in the shiny glass headquarters of the SEC, within arm’s reach of Chair Mary Jo White, and with more than enough empty seats to accommodate the President’s entire Cabinet and Senior Economic Advisors. He did so by seemingly dismissing the importance of an issue which, according to Dodd-Frank, the SEC was duty bound to reconsider – every four years – who would qualify as an accredited investor? And he did so in front of a gathering of people who had come from across the country to discuss and debate regulatory impediments to small business capital formation – with the definition of accredited investor being one of the three issues teed up by the Commission for discussion at the Forum. Yet instead of being met by jeers from the throngs that had gathered from across the country to discuss and debate this seemingly important issue – he was met with a round of applause.

To Commissioner Gallagher, the real issue was not simply the wisdom of spending Commission resources on revisiting the definition of “accredited investor.” Rather, the issue was one of priorities: Ought the Commission’s resources be overburdened with rulemaking dictated by Dodd-Frank, which had already overwhelmed the limited resources of the SEC – estimated to take at least an additional five years to complete? Or should the Commission be able to maintain its focus on protecting investors, maintaining orderly capital markets, and facilitating the flow of capital to those in the U.S. who needed it most in the midst and aftermath of The Great Recession – especially those businesses who are widely viewed as being the engine for job creation and economic growth – the American small business.

To Commissioner Gallagher, the real issue was not simply the wisdom of spending Commission resources on revisiting the definition of “accredited investor.” Rather, the issue was one of priorities: Ought the Commission’s resources be overburdened with rulemaking dictated by Dodd-Frank, which had already overwhelmed the limited resources of the SEC – estimated to take at least an additional five years to complete? Or should the Commission be able to maintain its focus on protecting investors, maintaining orderly capital markets, and facilitating the flow of capital to those in the U.S. who needed it most in the midst and aftermath of The Great Recession – especially those businesses who are widely viewed as being the engine for job creation and economic growth – the American small business.

In Gallagher’s view, it was the American small business which was most in need of the Commission’s resources and Congresses’ attention. And unlike the audience of thousands gathered in Marakech, Morocco for the Fifth Global Entrepreneurial Summit, judging by the applause those in the audience in the basement of 100 F Street, like Commissioner Gallagher, this Washington, D.C. audience grasped both the immediate mission at hand and its importance to the U.S. economy.

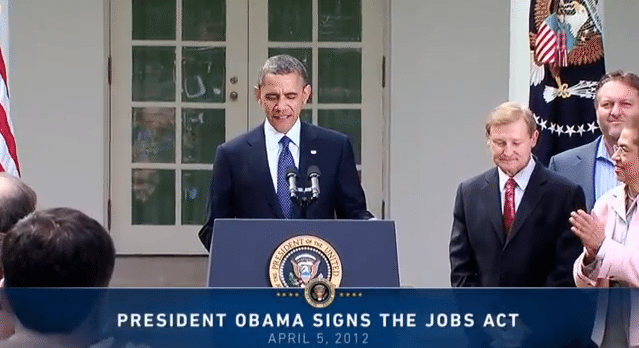

The Jumpstart Our Business Startups Act of 2012 (the “JOBS Act”) – Another Failed Promise?

There is nothing like an election year to help our Congress focus on issues that matter most to voters – and nothing garners votes better than the promise of more – and better paying – jobs. So in the spring of 2012 a normally divided Congress, together with the White House, rallied around a comprehensive patch quilt of legislation, ostensibly designed to improve the flow of capital to small and emerging businesses, with four of its principal sections stealing the spotlight: Title I, the so-called “IPO Onramp,” intended for companies to both stay private longer, and raise money from the public with  less burdensome SEC regulation; Title II, a provision intended to allow businesses large and small to publicly solicit investors in otherwise “private placements” to accredited investors; Title III, investment crowdfunding, bringing the Main Street world of Kickstarter and the like to Wall Street – to allow startups and small businesses to raise money from accredited and unaccredited investors, without registration, through internet solicitation, and Title IV, dubbed Regulation A+, intended to allow small and emerging businesses the opportunity to complete an IPO through a short form SEC registration, with lighter ongoing reporting, and without the entanglement of a maze of state blue sky regulations.

less burdensome SEC regulation; Title II, a provision intended to allow businesses large and small to publicly solicit investors in otherwise “private placements” to accredited investors; Title III, investment crowdfunding, bringing the Main Street world of Kickstarter and the like to Wall Street – to allow startups and small businesses to raise money from accredited and unaccredited investors, without registration, through internet solicitation, and Title IV, dubbed Regulation A+, intended to allow small and emerging businesses the opportunity to complete an IPO through a short form SEC registration, with lighter ongoing reporting, and without the entanglement of a maze of state blue sky regulations.

Was this to be a good law – or a bad law? Part of the answer lies in the question that New Deal President FDR posed to Ferdinand Pecora, a former Manhattan District Attorney and one of the first five SEC Commissioners, when FDR signed the Securities Exchange Act of 1934 into law:

“. . . now that I have signed this bill and it has become law, what kind of law will it be?” Replied Pecora, “It will be a good or bad bill, Mr. President,”depending upon the men who administer it.”

More than 2 ½ years after the enactment of the JOBS Act of 2012, not to mention a few SEC Chairs, the two titles of the JOBS Act focused exclusively on small business which are dependent on SEC rulemaking have yet to become operative, waiting on, among other things, a backlog of SEC rulemaking, including dozens of rules mandated by Dodd-Frank – none of which will ever help small business.

Whatever Happened to Small Business Capital Formation? – Commissioner Gallagher’s New Deal for America’s Small Businesses

In September 2014, at a major address delivered by Commissioner Gallagher at The Heritage Foundation in Washington, D.C., he spoke to what he believed the Commission’s priorities ought to be, and lamented the low priority historically afforded to small business in Washington, D.C.

In September 2014, at a major address delivered by Commissioner Gallagher at The Heritage Foundation in Washington, D.C., he spoke to what he believed the Commission’s priorities ought to be, and lamented the low priority historically afforded to small business in Washington, D.C.

“But small business has a big collective action problem here in Washington, where it is regularly and systematically underrepresented in the legislative and regulatory process. Small business owners are focused on making ends meet and growing their businesses, not hiring high-priced lobbyists to influence policy. Big businesses and unions, by contrast, can afford to hire lobbyists to develop relationships with politicians and regulators—which is the way business in the U.S. increasingly gets done.”

What followed in this speech was more akin to a Bill of Rights at the SEC for small business. Some of the points:

What followed in this speech was more akin to a Bill of Rights at the SEC for small business. Some of the points:

- Capital markets which are accessible to small business, with exemptions from registration and registration procedures suitable for small business, a la Regulation A+.

- Scaled disclosure for smaller reporting companies, including scaled accounting requirements.

- Secondary trading markets for smaller reporting companies which are tailored to the needs and requirements of early stage ventures and smaller emerging companies.

- Completion of Title III crowdfunding and Title IV Regulation A+ Rulemaking.

- Creation of an Office of the Small Business Advocate at the SEC.

- Greater attention by the Commission to statutes intended to protect small business in the rulemaking process, such as the Regulatory Flexibility Act of 1980.

Some Conclusions

It seems that in recent years our government in Washington, D.C. has lost its way in its pursuit of the American Dream – and the values that surround it. It was a rejection of excessive economic, political and social regulation, coupled with a healthy dose of what some might call greed, which drove the aspirations of early settlers of the U.S. and the generations that followed in their footsteps. And the risks they faced were not the ones that typically grace the pages of securities prospectuses today. Early Americans risked not only their life savings, but their lives and the lives of their families, in search of what most around the world look up to with hope and admiration – the American Dream.

With all due respect to Messrs. Dodd and Frank, for the sake of this generation, and generations of Americans to come, it is time to change the conversation in Washington, D.C., both in Congress and at the SEC, and to return to this country’s, and the SEC’s core priorities. And for those at the Commission, it is time to re-prioritize its Agenda – and move from being a  passive agency which in some important respects has lost its way, to a thought leader actively in pursuit of its core missions, with greater attention and focus on the most important job creator in this country – America’s small businesses.

passive agency which in some important respects has lost its way, to a thought leader actively in pursuit of its core missions, with greater attention and focus on the most important job creator in this country – America’s small businesses.

And if the fault lies with Congress, perhaps it is time for former U.S. Attorney Chair White to march over to Capitol Hill to answer for the Commission, from its perspective, questions in the vein similarly posed by FDR many years ago to another former government prosecutor: Were Dodd-Frank and the JOBS Act of 2012 a good law or a bad law?

___________________

Samuel S. Guzik, a Senior Contributor to Crowdfund Insider, is a corporate and securities attorney and business advisor with the law firm of Guzik & Associates, with more than 30 years of experience in private practice. A nationally recognized authority on the JOBS Act, including Regulation D private placements, investment crowdfunding and Regulation A+, he is and an advisor to legislators, researchers and private businesses, including crowdfunding issuers, service providers and platforms, on matters relating to the JOBS Act. As an advocate for small and medium sized business he has engaged with major stakeholders in the ongoing post-JOBS Act reform, including legislators, industry advocates and federal and state securities regulators. In 2014, some of his speaking engagements have included leading a Crowdfunding Roundtable in Washington, DC sponsored by the U.S. Small Business Administration Office of Advocacy, a panelist at the MIT Sloan School of Business 2014 Crowdfunding Roundtable, and a panelist at a national bar association event which included private practitioners, investor advocates and officials of NASAA. His articles on JOBS Act issues, including two published in the Harvard Law School Forum on Corporate Governance and Financial Regulation, have also served as a basis for post-JOBS Act proposed legislation. Recently he was cited by SEC Commissioner Daniel M. Gallagher in a public address for his advocacy on SEC regulatory reform for small business. He is admitted to practice before the SEC and in New York and California. Guzik has represented a number of public and privately held businesses, from startup to exit, concentrating in financing startups and emerging growth companies. He also frequent blogger on securities and corporate law issues at The Corporate Securities Lawyer Blog.

Samuel S. Guzik, a Senior Contributor to Crowdfund Insider, is a corporate and securities attorney and business advisor with the law firm of Guzik & Associates, with more than 30 years of experience in private practice. A nationally recognized authority on the JOBS Act, including Regulation D private placements, investment crowdfunding and Regulation A+, he is and an advisor to legislators, researchers and private businesses, including crowdfunding issuers, service providers and platforms, on matters relating to the JOBS Act. As an advocate for small and medium sized business he has engaged with major stakeholders in the ongoing post-JOBS Act reform, including legislators, industry advocates and federal and state securities regulators. In 2014, some of his speaking engagements have included leading a Crowdfunding Roundtable in Washington, DC sponsored by the U.S. Small Business Administration Office of Advocacy, a panelist at the MIT Sloan School of Business 2014 Crowdfunding Roundtable, and a panelist at a national bar association event which included private practitioners, investor advocates and officials of NASAA. His articles on JOBS Act issues, including two published in the Harvard Law School Forum on Corporate Governance and Financial Regulation, have also served as a basis for post-JOBS Act proposed legislation. Recently he was cited by SEC Commissioner Daniel M. Gallagher in a public address for his advocacy on SEC regulatory reform for small business. He is admitted to practice before the SEC and in New York and California. Guzik has represented a number of public and privately held businesses, from startup to exit, concentrating in financing startups and emerging growth companies. He also frequent blogger on securities and corporate law issues at The Corporate Securities Lawyer Blog.