OTC Markets Questions Monopoly Model for Venture Exchange.

The House Financial Services Committee has been busy once again with a slew of proposed laws designed to improve the environment for smaller companies. One of the bills on the list for the Committee yesterday (March 2, 2016), was the Main Street Growth Act (HR 4638), introduced by Representative Scott Garrett from New Jersey. This act of legislation would potentially enable venture exchanges and hopefully reinvigorate the moribund IPO market for smaller companies (SMEs).

The House Financial Services Committee has been busy once again with a slew of proposed laws designed to improve the environment for smaller companies. One of the bills on the list for the Committee yesterday (March 2, 2016), was the Main Street Growth Act (HR 4638), introduced by Representative Scott Garrett from New Jersey. This act of legislation would potentially enable venture exchanges and hopefully reinvigorate the moribund IPO market for smaller companies (SMEs).

The subject of Venture Exchanges has been a hot topic on Capitol Hill as well as at the F Street offices of the SEC. There is a growing recognition among appointed, and elected officials, that public markets are not quite right. Fewer Initial Public Offerings (IPOs) are happening as companies remain private for as long as possible. While there are various reasons for promising companies to remain private, one of the biggest issues is the cost, and scrutiny, associated with trading shares on a public exchange. While the private markets (IE Reg D) are huge, at over $1 trillion per year, IPOs have dwindled to just a trickle. In 2015 according to this report, fewer companies went public than any other time since 2009 raking in just $30 billion.

In a presentation at the SEC last year by David Weild, former Vice Chair of Nasdaq, data was delivered that should cause concern for all:

In a presentation at the SEC last year by David Weild, former Vice Chair of Nasdaq, data was delivered that should cause concern for all:

- The number of listed companies has declined from 9,000 to approximately 5000

- US fell from #1 to 12th place for smaller Initial Public Offerings

- The US fell to 2nd place for large IPOs

And why does this all matter? Jobs. Economic growth. Opportunity for all.

Venture exchanges are a logical extension of the JOBS Act of 2012. While the JOBS Act legislation attempted to craft regulations that provide greater access to capital for smaller companies, the bill was void on the topic of creating a liquid and vibrant secondary market for the trading of these securities. Companies that take advantage of various aspects of the JOBS Act may look to a venture exchange to provide sellers the opportunity to exit, and investors the chance to purchase, equity in a smaller company if they choose to list their shares.

The bill as submitted passed the House Financial Services Committee and is embedded below. The concept captured bipartisan support that was not represented in the final vote.

Representative Maxine Waters, ranking Democrat on the Committee, requested more time to study, and review, the proposal and submitted an amendment to the bill that was subsequently denied.

Representative Maxine Waters, ranking Democrat on the Committee, requested more time to study, and review, the proposal and submitted an amendment to the bill that was subsequently denied.

Waters stated;

“I am not rejecting the concept but none of us really understand how this will work … I like the concept. I believe there is value. Let’s understand it. Let’s get a bipartisan effort going.”

While explaining the “language is not set in stone”, Representative Garrett made the statement;

“The SEC has had 82 years to do this. If not us – who, If not now – when?“

OTC Markets, an entity that has positioned itself to be the venture exchange for the United States, expressed their consternation that the proposal may create a monopoly as opposed to a competitive environment for exchanges to evolve.

OTC Markets sent a letter to the Committee (embedded below) earlier this week presenting their position. In brief, OTC Markets is of the opinion;

OTC Markets sent a letter to the Committee (embedded below) earlier this week presenting their position. In brief, OTC Markets is of the opinion;

We generally support legislation aimed at improving the secondary trading of smaller company securities, however the Main Street Growth Act falls short. The bill would allow the creation of “Venture Exchanges” that are intended to have trading and listing rules tailored for smaller companies and regulatory privileges that are unavailable to non-exchange markets. The bill solely focuses on the exchange model, excluding other successful markets that currently operate venture and smaller company markets.

The bill’s prescription of a single, centralized, exchange-only monopoly business model does not take into account the lessons to be learned from:

- the historical success of the NASDAQ market maker driven automated quotation system for smaller companies;

- OTC Markets Group in the U.S. today, which is the global leader in exchange graduates with over 200 companies moving to the NYSE or NASDAQ exchanges in the past three years; and

- other successful smaller company markets around the world, such as the AIM in London or China’s fast growing NEEQ1, that support networks of competing broker-dealers supplying liquidity and execution services.

Cromwell Coulson, CEO of OTC Markets shared in an email his opinion;

Cromwell Coulson, CEO of OTC Markets shared in an email his opinion;

Ultimately, small companies should be free to choose their listing venue based on value and cost, while broker-dealers should be free to seek best execution from the market or broker-dealer of their choice. Forcing these participants to use a venue type prescribed by regulators is not in the best interest of the small company trading market.

Understandably, OTC Markets supported the Waters amendment that was voted down.

Recently, in one of the earliest IPOs of 2016, Elio Motors, a company that raised capital under Reg A+ (Title IV of the JOBS Act) successfully listed on the OTCQX (OTC’s best market). Representative Waters touted this as indicative of what OTC Markets has already accomplished – and could achieve going forward.

Where does this all go? To the floor of the House for a vote at some point in the future and then off to the Senate.

While the specifics of the Bill may change (and thus perhaps mollify OTC’s concerns) the proposal is profoundly important. Garrett along with other Committee members are pursuing an important policy issue: facilitating access to capital for smaller companies while providing access to investment opportunity for smaller investors (not just big money).

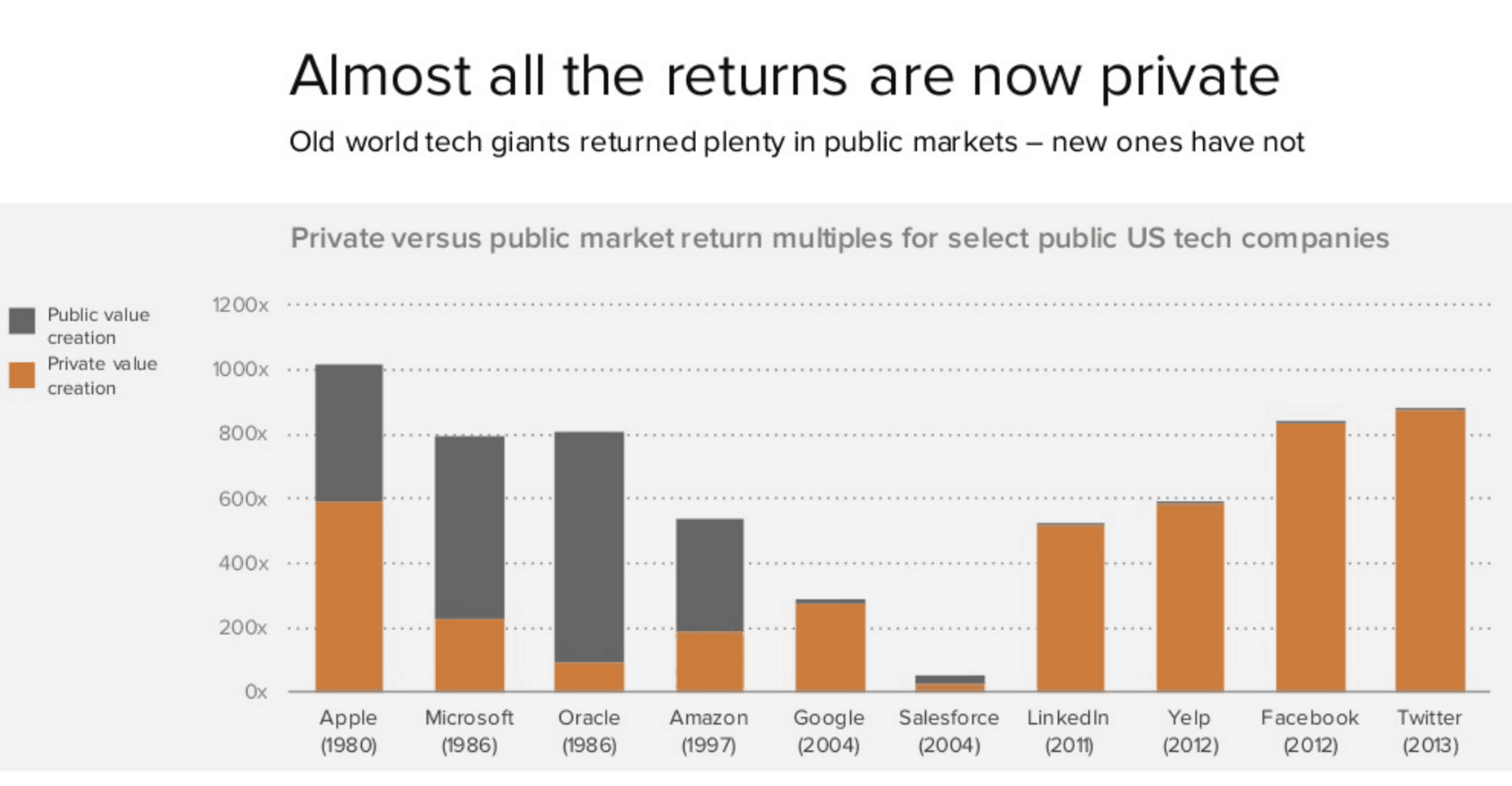

As promising small companies have avoided going public the best of the best have not had any problem raising capital.

As promising small companies have avoided going public the best of the best have not had any problem raising capital.

Venture Capital, family offices, and other wealthy types have always had access to invest in the Uber’s of the world (prior to being anointed Unicorn status). The situation has become so dire that today, almost all returns (capital gains) are scooped up prior to listing on a public exchange. In some respects, an IPO has become an exit event and not a good investment opportunity. At least not for the masses.

[scribd id=302035867 key=key-1QSU5MO8pMVYv4nr7b5B mode=scroll]

[scribd id=302036050 key=key-XsvcUo6z8skmmnyDB9mF mode=scroll]