Big consultancies, such as PwC, Cap Gemini, KPMG, Deloitte and Accenture, research and analyze fintech developments to support the digital transformation of their banking customers. They promote this work through well-crafted free reports and white papers. The latest of such reports was published by Julian Skan, Senior Managing Director and Eve Ryan, Banking Research Lead in the UK & Ireland Financial Services division of Accenture UK under the provocative title: “Did someone cancel the Fintech revolution?”

This report argues that fintech ventures have so far failed because of a lack of investment and that banks can, and should, take the lead in the fintech revolution by investing more and differently.

Far from being as polemic as its title might suggest, the report reflects the consensus among banking consultants. A consensus also often shared among fintech professionals, for example at recent conferences in Paris and Berlin. The narrative of the consensus goes as follows: Banks are here to stay because they have deep pockets and entrenched relationships. Fintech startups don’t. Their customer acquisition costs are too high and VC money doesn’t go the distance. Hence, fintech ventures can’t make it alone. Rather than attempting to be a challenger bank, a financial portal or any sort of financial destination site, fintech ventures should slip into the role of bank enablers. Fintechs and banks’ collaboration is best for both.

Like often in finance, it’s important to question the consensus. In what follows we question three claims of this report.

Claim No. 1: The Fintech revolution has stalled

Accenture UK’s report paints a pretty grim picture of what the Fintech revolution has achieved so far. It claims that both Fintech startups and bank-incubated ventures have failed to deliver. As the authors put it:

“There are indications the Fintech revolution has stalled. It promised to change market structure, to radically improve products and services, and to save the incumbent banking sector from a slow slide to invisible utility status. But these promises are yet to come to pass.”

![]()

![]()

According to the authors, the Fintech revolution failed to create enough value and to create it fast enough.

The claim is supported by a few examples rather than statistics. UK retail banking Fintechs such as Revolut seem to be “perpetually stuck in beta”. Wealth management Nutmeg (40,000 users) and challenger bank N26 (300,000 users in 2 years) “failed to capture the market.“ Their customer acquisition costs largely outweigh the cost advantage of not having physical branches. Building a full-service bank and a balance sheet should take challenger banks 15 to 20 years.

Internal banking teams have not fared better.

“Internal incubators and innovation streams have universally failed to produce killer apps. Death after proof of concept has become the norm.”

The authors see a confirmation of their claim that Fintech is wavering in the significant slowdown of UK fintech investments by VCs. It went down by 36%, from $1.1 billion in 2015 to $0.7 billion in 2016.

Counterargument/Food for thought

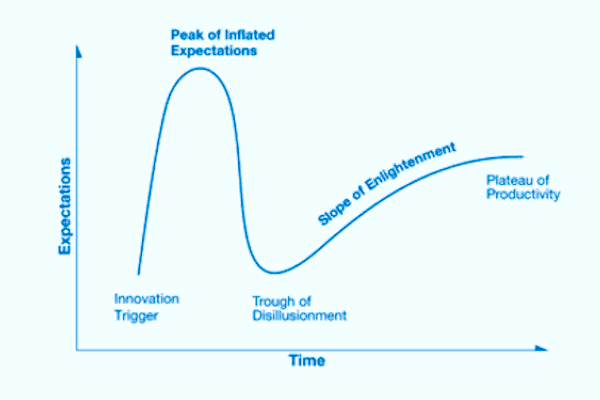

Fintech ventures are precisely that: ventures. Many will fail before one can tell that the survivors succeeded. As investments come in cycles, the first wave of inflated expectations is followed by failures and a trough of disillusionment, as depicted in the Gartner Group’s Hype Cycle.

Sweeping judgments about Fintech ventures at large can be very misleading. In online “winners-take-all” markets, a few successful firms can disrupt an entire sector. Think Amazon, Airbnb, Booking.com, Netflix etc.

Bankers often argue that finance is different as it does not tolerate monopolies. In practice, however, finance lives under the yokes of the GAAFA (Google, Apple, Amazon, Facebook, Alibaba), like any other industry does. Finance and insurance companies are the top ad spenders on Google Search (86% of UK market). Banks should not think that they are immune to the arrival of a predator à la Uber, able to raise billions of dollars ($8.8 in equity plus $3 billion+undisclosed in debt) to gain market share. Even if Uber ultimately fails, it will have ruined many incumbent transporters in the process.

Bankers often argue that finance is different as it does not tolerate monopolies. In practice, however, finance lives under the yokes of the GAAFA (Google, Apple, Amazon, Facebook, Alibaba), like any other industry does. Finance and insurance companies are the top ad spenders on Google Search (86% of UK market). Banks should not think that they are immune to the arrival of a predator à la Uber, able to raise billions of dollars ($8.8 in equity plus $3 billion+undisclosed in debt) to gain market share. Even if Uber ultimately fails, it will have ruined many incumbent transporters in the process.

Lastly, contrary to what the report states, UK Fintechs like Transferwise and lending startups like Funding Circle are unicorns who meet several of the stated metrics of Fintech success:

- Radically more efficient business models showing 20% to 30% cost improvement.

- Increased competition, price decreases, greater price transparency and more switching.

- New ‘surprise and delight’ customer experiences.

- Net new revenue and valuations that reflect this – > 20 Price/Earnings ratio.

Claim No. 2: Fintech is too “tech-light”

According to the authors, next to the cost of customer acquisition and compliance, a major reason why Fintech is stalling is that investment in the new technologies – the technology of the past 10 years that define the Fintech revolution – has been too low.

“Fintech’s failure thus far to contribute meaningfully to productivity has been driven by a slow start to investment.”

Many Fintech ventures have no competitive technology advantage over incumbents:

“The household names in the Fintech business today make only light or early-stage use of the latest technologies. And some use none at all, and are deploying legacy technology to deliver new products or reach new customer segments.”

This holds of alternative lending:

“These [alternative lending] models have already been embraced by incumbents, they only make light use of new technology. They can hardly therefore be said to represent a revolution in the marketplace.”

This is also true of China’s Fintech hub which, in spite of the success Chinese Fintech giants like Alipay and JD Capital (445 million and 226 million, customers respectively) is not, according to the authors, a model of sustainable value creation because its success is not built on efficient systems and advanced technology.

Counterargument/Food for thought

It is indeed startling for outside observers how low-tech some tech startup can be in their early stage.

Yet, Amazon did not start with a $2 billion automated warehousing facility. It did build one as soon as it could. Likewise, starting from scratch, Fintech startups generally focus their early technology advantage on a few front- end technologies. They often operate their back office in the existing ecosystem, which contributes to their high operating costs. As they gain traction, however, they entice other startups to build an alternative ecosystem of more efficient and less costly solutions. Payment startups such as Transferwise, Kantox, or Adyen, for example, enable banking and lending startups.

end technologies. They often operate their back office in the existing ecosystem, which contributes to their high operating costs. As they gain traction, however, they entice other startups to build an alternative ecosystem of more efficient and less costly solutions. Payment startups such as Transferwise, Kantox, or Adyen, for example, enable banking and lending startups.

Lastly, if Fintech ventures are technology light, banks are indeed “technology heavy”, plagued by their legacy systems. Fintech startups are free of such a burdens and can go a long way using nimble technologies such as agile Web development and open API technologies.

Claim No. 3: Banks can and should drive the Fintech revolution forward

The report goes on to claim that banks must be the ones who drive forward the Fintech revolution that has stalled for lack of VC funding.

“Getting banks to realize the potential upside of the innovative, game-changing technologies already available would be the first step in breaking this [down] cycle.”

Banks must act in any case, irrespective of the Fintech competition. Changes in economics, customer needs and regulation drive profound changes in the structure of the financial services market. Vertically integrated banks are threatened by a proliferation of new businesses providing customer access to financial services – separating customer experiences and access from manufacturing, infrastracture and connectivity. A process often called “unbundling the bank.”

To unlock the potential of value creation trapped in Fintech, banks must up their investments. The authors qualify as “relatively low” the cumulative investment of $500 million by Barclays’, HSBC’s, and Santander’s technology funds since 2014.

UK banks should not only invest more, they should invest better, which means investing in:

- Innovative enabling technologies such as Blockchain.

- Late-stage Fintech startups that would bring to banks the benefits of VC’s investment.

- Exportable category killers such as payment Fintechs VocaLink (now a Mastercard company) and Worldpay. Fintech killer software, for example, would enable banks to conquer new geographies such as Mexico, Russia and China and new segments such as the 2 billion unbanked people worldwide. These investments would be more profitable than trying to make the domestic UK banking market more efficient and competitive, which is a zero-sum game.

In addition, the UK banking sector should continue to seek the support of the UK regulator and to build Fintech bridges with countries like China, Singapore and Australia in order to mitigate the impact of the Brexit.

Counterarguments/Food for thought

As it tries to show how the UK banking sector, one of the largest in the world relative to GDP, should reassert its leadership and “punch above its weight,” the authors reveal how low a potential they see for value creation in the domestic UK banking market:

“This [strategy of investing in Fintech exports] will offer a far greater return than simply making a domestic market a better version of its current self.”

Yet, customers want better customer experiences and banks have no choice but to defend their turf. Considering the previously disrupted markets like the media and eCommerce, one can anticipate that the so-called zero-sum game between Fintech and banks in the UK soon experiences a drastic acceleration of the destruction of value for incumbent banks.

[clickToTweet tweet=”Domestic banking could soon experience a drastic acceleration of destruction of value #Fintech” quote=”Domestic banking could soon experience a drastic acceleration of destruction of value #Fintech”]

As timing is everything in tech, a strategy of investing in late-stage innovative startups could prove difficult as these will be highly visible and expensive. Mastercard paid more than £700 million to acquire 9-year old VocaLink. BNP Paribas in France was wise enough to acquire neo-bank Compte Nickel for an undisclosed amount as it was hardly 3 years old.

Whether Fintech ventures are internal or external, early-stage or late-stage, bound for export or domestic market, will matter little in the end. The decisive factor will be the cultural and organizational ability of banks to let these ventures thrive. And that is their major weakness. Banks will find it very hard to become the Amazon Web Services of finance. It is doubtful that their shareholders will allow them to invest the billions of dollars that it would take.

Conclusion

In conclusion, like others of its kind, this short but dense report by Accenture UK offers much food for thought. It tries to defend a bank-centric view of Fintech. In doing so, it shows that the Fintech game is a hard one to play and that it is also an inescapable one.

Therese Torris, PhD, is a Senior Contributing Editor to Crowdfund Insider. She is an entrepreneur and consultant in eFinance and eCommerce based in Paris. She has covered crowdfunding and P2P lending since the early days when Zopa was created in the United Kingdom. She was a director of research and consulting at Gartner Group Europe, Senior VP at Forrester Research and Content VP at Twenga. She publishes a French personal finance blog, Le Blog Finance Pratique.

Therese Torris, PhD, is a Senior Contributing Editor to Crowdfund Insider. She is an entrepreneur and consultant in eFinance and eCommerce based in Paris. She has covered crowdfunding and P2P lending since the early days when Zopa was created in the United Kingdom. She was a director of research and consulting at Gartner Group Europe, Senior VP at Forrester Research and Content VP at Twenga. She publishes a French personal finance blog, Le Blog Finance Pratique.

[scribd id=350636076 key=key-TVkJgAJh3bTmu2sP5J8t mode=scroll]