Last week, equity crowdfunding platform Seedrs offered shares to their broader audience as part of a funding round to raise £10 million. According to the platform, £2.5 million in equity was made available for registered investors on its site. This is not the first time Seedrs raised capital on its own platform – and it is probably not the last.

Last week, equity crowdfunding platform Seedrs offered shares to their broader audience as part of a funding round to raise £10 million. According to the platform, £2.5 million in equity was made available for registered investors on its site. This is not the first time Seedrs raised capital on its own platform – and it is probably not the last.

Gonçalo de Vasconcelos, CEO of competing platform SyndicateRoom, released a statement on the funding round;

“I’m pleased to see that Seedrs successfully completed their own raise today. It shows the progress and growing maturity of the equity crowdfunding industry in the UK.

However it’s disappointing to note that the institutional investors are receiving preferential shares whilst the crowd is not, effectively treating the crowd as second class citizens. This is something SyndicateRoom has long been advocating against. To make equity crowdfunding truly equitable we believe that all investors in the round should have access to the same class of shares and same price per share, which is exactly what happens at SyndicateRoom.”

Crowdfund Insider reached out to Seedrs for clarification on the share structure and received a response that investors were acquiring the same ordinary shares that founders, and all other shareholders, received with the exception of two institutions which received Series A preferred. New investors did receive EIS tax treatment, which is advantageous, whereas the preferred shares did not. The preferred shareholders did receive some “limited downside protection”. This was all made clear to the individuals who participated in the offer.

Crowdfund Insider reached out to Seedrs for clarification on the share structure and received a response that investors were acquiring the same ordinary shares that founders, and all other shareholders, received with the exception of two institutions which received Series A preferred. New investors did receive EIS tax treatment, which is advantageous, whereas the preferred shares did not. The preferred shareholders did receive some “limited downside protection”. This was all made clear to the individuals who participated in the offer.

This is an interesting polemic on a broader basis as the type of share you purchase does count. Different share types exist in both private and public markets. It’s a pretty common thing. While most platforms allow the issuer to decide the share structure, SyndicateRoom has, to date, consistently affirmed that all shareholders are treated exactly the same. Seedrs, for its part, has emphasized the importance of small shareholders receiving equivalent rights to larger investors. According to their site;

“Regardless of how you invest, at Seedrs we believe that the smallest investors should have the same rights as even the largest investors and that is why only A shares, with full voting rights, are offered to all investors.”

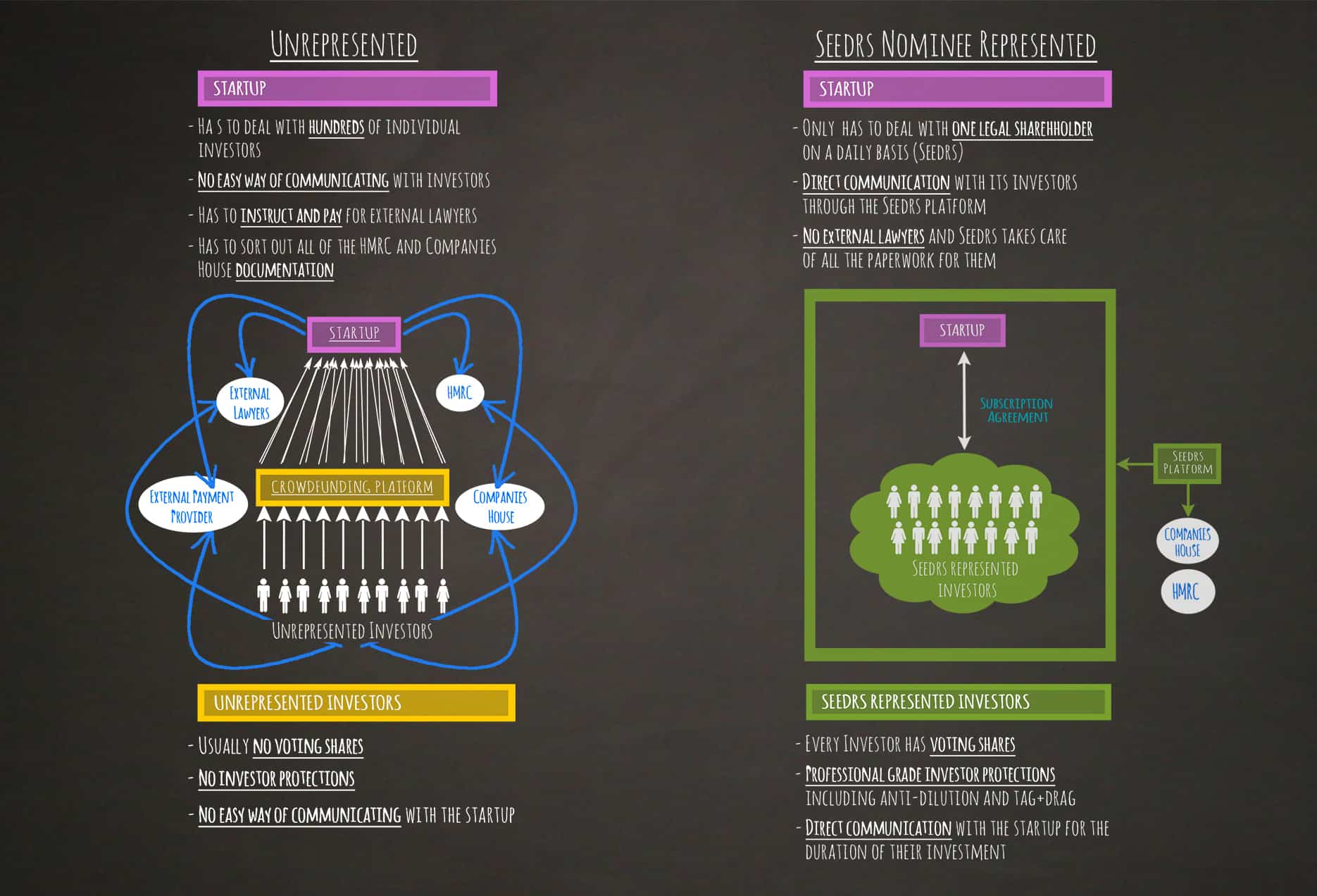

So far, outside of a few exceptions, Seedrs has remained true to this claim. Seedrs has also embraced a “nominee structure” where Seedrs actually holds legal title to the shares on behalf of the investor. You may read more about their philosophy here.

Some industry followers have been critical of crowdfunding platforms that leave smaller shareholders at risk to significant dilution. This FT article addressed part of the challenge in the evolving industry.

In the end, the most important point is that each investor clearly understands the risk associated with their investment, and the structure of the security, along with the rights incumbent to the shareholder. Most investment crowdfunding platforms strive for transparency and fluid communication between issuer, investor and platform – something that needs to be lauded and encouraged.