Monday, May 16, 2016 is the first day that ordinary people—not just the super rich—will be able to invest in the next Uber or Snapchat. That’s because Title III of the JOBS Act, otherwise known as Regulation Crowdfunding or Reg CF, legalizes retail investment crowdfunding that day. This new regulation will open up the investor pool to over 300 million potential investors and aims to spur the growth of small businesses.

The Long Road to Investment Crowdfunding

In April 2012, President Barack Obama signed into law the Jumpstart Our Business Startups Act, or JOBS Act. The JOBS Act was so called because it aimed to facilitate access to capital for startups and small businesses, give more people the ability to participate in investment opportunities, and ultimately, create more jobs and stimulate economic growth. While other crowdfunding regulations from the JOBS Act, such as Title II and IV, were implemented more quickly, Title III is the third but most anticipated piece of crowdfunding regulation to become effective.

In April 2012, President Barack Obama signed into law the Jumpstart Our Business Startups Act, or JOBS Act. The JOBS Act was so called because it aimed to facilitate access to capital for startups and small businesses, give more people the ability to participate in investment opportunities, and ultimately, create more jobs and stimulate economic growth. While other crowdfunding regulations from the JOBS Act, such as Title II and IV, were implemented more quickly, Title III is the third but most anticipated piece of crowdfunding regulation to become effective.

For the first time, Title III will allow issuers to raise funds online from ordinary people for investment purposes. The regulation creates a new exemption to the Securities Act of 1933. This essentially means that, for the first time since being written 80 years ago, our securities laws will be updated to recognize modern modes of online capital raising.

Previously, generally only accredited investors could invest in early stage startups. Accredited investors are those who earn an annual income of at least $200,000 (or $300,000 if married), or those with a net worth of at least $1M (excluding one’s primary residence).

Going Beyond Kickstarter or GoFundMe Campaigns

You might argue that crowdfunding has been around for years now, which is true. Crowdfunding is essentially the act of raising capital from others via the Internet. Platforms like Kickstarter, IndieGogo, and GoFundMe have been around since at least 2008 and have given us the Pebble Watch, Veronica Mars, and every gadget imaginable. However, these portals practice rewards-based crowdfunding, or in the case of GoFundMe, donation-based crowdfunding. When backers give a crowdfunding campaign money, they either make a donation or get back a “reward”—maybe a thank you note, or the first edition of said widget.

You might argue that crowdfunding has been around for years now, which is true. Crowdfunding is essentially the act of raising capital from others via the Internet. Platforms like Kickstarter, IndieGogo, and GoFundMe have been around since at least 2008 and have given us the Pebble Watch, Veronica Mars, and every gadget imaginable. However, these portals practice rewards-based crowdfunding, or in the case of GoFundMe, donation-based crowdfunding. When backers give a crowdfunding campaign money, they either make a donation or get back a “reward”—maybe a thank you note, or the first edition of said widget.

Title III expands the possibilities to include investment crowdfunding, or the ability to buy equity in an early stage company and hopefully reap a monetary return on investment. On May 16, ordinary Americans don’t need to settle for just a Pebble watch (though that would be a great additional perk); instead, they can own a piece of the company that makes the Pebble watch. Title III democratizes access to startup investment opportunities, while greatly expanding the pool of available capital to small businesses and startups. And while the crowd may not replace angel investors and venture capital, they may now invest alongside them.

Here’s What You Need to Know

Issuers, or those looking to raise funds, should know the following basics about Title III:

- You may only raise $1M in a rolling 12-month period

- You must use an online intermediary (more on this below)

- You must be a U.S. entity

- You must disclose certain financial information, and depending on how much you plan to raise, your financial statements may need to be reviewed or audited by an accountant

- You must fulfill certain ongoing reporting requirements

- You may raise funds from both accredited and non-accredited investors, although investors are limited to investing a certain dollar amount based on their income or net worth.

Title III is historic in that it specifically recognizes a new type of intermediary for crowdfunding transactions, called a funding portal. At least 30 applications for funding portals have been received as of April, with likely many more to come. Funding portals are essentially modern online connectors between issuer companies and investors and amongst investors, and these platforms will be regulated by the SEC and FINRA.

But It Wont Be A Smooth Liftoff

Despite high hopes around a vibrant Title III crowdfunding industry, Title III may encounter some turbulence at takeoff following its May 16 debut. Although it took the SEC three and a half years to issue the final rules on Title III, regulators were said to be scrambling in the final days of the regulatory process to get the final rules out. And in doing so, the final rules came out short of optimal and, in the opinion of some, not workable.

Despite high hopes around a vibrant Title III crowdfunding industry, Title III may encounter some turbulence at takeoff following its May 16 debut. Although it took the SEC three and a half years to issue the final rules on Title III, regulators were said to be scrambling in the final days of the regulatory process to get the final rules out. And in doing so, the final rules came out short of optimal and, in the opinion of some, not workable.

Critics point out that the SEC’s final rules on Title III do just the opposite of its regulatory intent. That is, instead of creating a mechanism that would allow attractive startups to include retail investors, the SEC’s zealous concerns over small investor protection resulted in unrealistically high regulatory burdens that would disincentivize any company from using the regulation, except as a last resort. And that’s the opposite of what small investors should want to invest in—the companies otherwise rejected by accredited investors.

High Costs and Low Success Rate

One of the major concerns around Title III is the high transaction costs required to raise $1M. Issuers will find themselves with bills in the tens of thousands of dollars right out of the gate to pay for legal and accounting services—and will then have to spend at least a couple thousand dollars after fundraising to comply with ongoing reporting requirements. Several industry experts have publicly criticized the final rules, including OneVest/1000 Angels co-founder and Chairman Alejandro Cremades who issued an open letter condemning Title III and publicly stating that his company would stay “far away” from utilizing the regulation.

Even with low cost solutions like iDisclose and Crowdcheck, the upfront costs to conduct financial audits—before an issuer may even determine whether it will be able to raise financing at all—is a gamble.

And issuers must all the while acknowledge the likelihood that its campaign will fail. If we take lessons from analogous models, Kickstarter has a 36% success rate for fully funded campaigns, while AngelList has testified that less than 10% of companies that list on its platform succeed in a raise. Some platforms that lean towards “listing” rather than “curating” may find that very few campaigns overall will reach their funding goal. Issuers will want to ensure that they surround themselves with good advisors and counsel, and to associate themselves with well-performing funding portals, or else they may find themselves in the red if they’ve raised less money than needed to even cover transaction costs.

But It’s Not Dead Yet

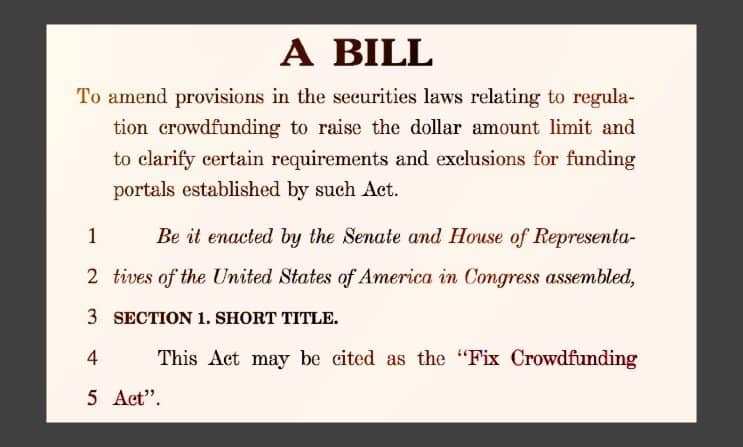

Currently, Congressman McHenry has introduced proposed legislation called the Fix Crowdfunding Act (HR 4855) that has yet to be voted on by the House or Senate. The amendment fixes a number of issues with Title III to make it more workable, if approved and implemented. HR 4855 makes the following changes:

Currently, Congressman McHenry has introduced proposed legislation called the Fix Crowdfunding Act (HR 4855) that has yet to be voted on by the House or Senate. The amendment fixes a number of issues with Title III to make it more workable, if approved and implemented. HR 4855 makes the following changes:

Testing the Waters

Issuers would be able to solicit interest prior to actually spending money on lawyers and accountants. Given that companies must brace themselves for the scenario in which they cannot cover transaction costs or loss money as a result of not having raised enough funds, the ability to gauge investor interest up front may save a number of issuers from being in the red on day one (and may encourage other companies to boldly steam forward).

Raising the Funding Cap From $1M to $5M

In his open letter, Cremades wrote “Nowadays startups on average raise, at a Seed stage, in the neighborhood of $2M+. The fact that startups will have a limit of $1M per year will either force them to be under capitalized or conduct another type of offering in parallel to raise the remaining capital from accredited investors, which means more costs from a legal perspective.” Raising the funding cap to $5M would make the transaction costs more justifiable and allow companies to raise the capital they need.

Funding Portal Curation and Liability

Funding portals are the first line of defense against fraud, and have the challenge of proving to regulators and investors that they can effectively detect and combat fraud. There have already been enforcement actions against other crowdfunding campaigns, including the FTC’s investigation against Erik Chevalier (fraud on Kickstarter) and SEC’s charges against Ascenergy (fraud in accredited investment crowdfunding). To combat fraud, many funding portals plan to conduct due diligence on issuers and curate the campaigns they accept on their platforms.

Funding portals are the first line of defense against fraud, and have the challenge of proving to regulators and investors that they can effectively detect and combat fraud. There have already been enforcement actions against other crowdfunding campaigns, including the FTC’s investigation against Erik Chevalier (fraud on Kickstarter) and SEC’s charges against Ascenergy (fraud in accredited investment crowdfunding). To combat fraud, many funding portals plan to conduct due diligence on issuers and curate the campaigns they accept on their platforms.

Although funding portals are allowed to curate and vet the campaigns they accept onto their portal, HR 4855 bolsters this aspect by clarifying that funding portals may refuse to work with companies that make false statements, omit material facts, or engage in fraudulent or deceitful conduct. This clarity is helpful because funding portals are not allowed to give investment recommendations or advice; there is some confusion at the moment as to what extent representations of curation by funding portals may be deemed to be investment advice or recommendations.

Under the current Title III rules, the issue of funding portal liability is unclear. In its final rules, the SEC stated:

“We are specifically declining to exempt funding portals (or any intermediaries) from the statutory liability provision of Section 4A(c) or to interpret this provision as categorically excluding such intermediaries. We do not believe that we should preclude the ability of investors to bring private rights of action against funding portals (or any intermediaries).”

Unfortunately, this makes funding portals a prime target of plaintiff’s counsel for deals that go sideways—especially if the issuer is no longer around. HR 4855 adds language to clarify that funding portals will not share in issuer liability unless they knowingly make an untrue statement, omit material facts, or engage in fraudulent or deceitful conduct. If passed, funding portals may breathe a small sigh of relief in not being subjected to overwhelming liability and potentially endless litigation by investors.

Interestingly, drafters also added a clause allowing funding portal relief from any enforcement action until 2021. Whether that clause will survive the legislative process remains to be seen, but if it does, funding portals will be able to take more (hopefully, calculated) risks while waiting for SEC guidance to come out on thorny issues.

SPVs to Consolidate Cap Tables

Under the current rules, Title III does not allow for special purpose vehicles (SPVs). However, HR 4855 would enable companies to use SPVs for more efficient capital raising.

SPVs allow issuers to consolidate multiple investors into one entity. Typically, an issuer negotiates terms with a lead investor and any other investor wanting to join the funding round does so on the same terms as the lead investor. These follow-on investors will buy equity in an SPV, which becomes the one consolidated investor in the company. This way, issuers can avoid having to manage tens or hundreds of investors on their cap table, chase around individual investors, and can spend more time working on their business rather than dealing with the administration and management of individual investors. Anecdotally, venture capitalists are said to shy away from companies with lengthy cap tables.

Removing Future Public Registration

HR4855 removes a provision requiring companies to register and begin reporting under the Exchange Act, similar to that of a public company, within 2 years of exceeding $25 million in assets if the company has 500 or more non-accredited investors. If a platform plans to raise the maximum funding amount of $1 million, it would have to require investment minimums of at least $2000 from each non-accredited investor in order to avoid this requirement—a hefty minimum investment amount for someone who isn’t accredited. As AngelList COO and CIO Kevin Laws explained to Congress, this reporting requirement “would dissuade later investors from investing in fast-growing companies if doing so would put the company in a 24-month path to meeting public company requirements; the very companies that [need?] the money most to grow would be dissuaded from raising because of [this] registration requirement.”

Other Proposed Changes

Other proposed changes to the crowdfunding regime are in the works. One notable example is the Supporting America’s Innovators Act of 2016 (HR 4854), which solves the “99 investor problem.” Under the Investment Company Act, an “investment company” is an issuer which is or holds itself out as being engaged primarily, or proposes to engage primarily, in the business of investing, reinvesting or trading in “securities.” To avoid registration and the burdensome requirements that come with it, companies seeking to claim the Section 3(c)(1) exemption may only be owned by up to one hundred persons. This poses serious issues in crowdfunding, where fundraising efforts rely on smaller investments by a larger number of investors. Similar to the SPV discussion above, companies often form LLC to avoid a drain on resources, administrative burdens to the company, and having to chase around tens or hundreds of investors for signatures. However, the 99 investor limit often results in money being left on the table and acceptance of only the 99 highest funding commitments. This archaic rule works against crowdfunding, the main point of which is diversification, allowing more investors in smaller investment amounts, and the inclusion of retail investors.

Other proposed changes to the crowdfunding regime are in the works. One notable example is the Supporting America’s Innovators Act of 2016 (HR 4854), which solves the “99 investor problem.” Under the Investment Company Act, an “investment company” is an issuer which is or holds itself out as being engaged primarily, or proposes to engage primarily, in the business of investing, reinvesting or trading in “securities.” To avoid registration and the burdensome requirements that come with it, companies seeking to claim the Section 3(c)(1) exemption may only be owned by up to one hundred persons. This poses serious issues in crowdfunding, where fundraising efforts rely on smaller investments by a larger number of investors. Similar to the SPV discussion above, companies often form LLC to avoid a drain on resources, administrative burdens to the company, and having to chase around tens or hundreds of investors for signatures. However, the 99 investor limit often results in money being left on the table and acceptance of only the 99 highest funding commitments. This archaic rule works against crowdfunding, the main point of which is diversification, allowing more investors in smaller investment amounts, and the inclusion of retail investors.

Thomson Reuters Practical Law is collaborating with Crowdfund Insider on a series of articles about the recent regulatory changes in the crowdfunding industry. The themes include JOBS Act Title III overview, global regulatory framework, and future regulatory improvements for existing crowdfunding regimes. The views expressed by the authors of these articles do not necessarily represent the views of Thomson Reuters nor any of its affiliates.

Amy Wan is a Contributor for Crowdfund Insider. She is Principal at The Law Office of Amy Wan, Esq., where she advises on startup and crowdfunding law. Formerly, she was General Counsel at Patch of Land, a real estate marketplace lending platform. While there, Amy pioneered the industry’s first payment dependent note that is secured pursuant to an indenture trustee and designed to be bankruptcy remote, and advised the company on its $20.4M Series A funding round. She was recognized as a Finalist for the Corporate Counsel of the Year Award 2015 by LA Business Journal. She is the founder and co-organized of Legal Hackers LA, and was named one of the one of ten women to watch in legal technology by the American Bar Association Journal in 2014.

Amy Wan is a Contributor for Crowdfund Insider. She is Principal at The Law Office of Amy Wan, Esq., where she advises on startup and crowdfunding law. Formerly, she was General Counsel at Patch of Land, a real estate marketplace lending platform. While there, Amy pioneered the industry’s first payment dependent note that is secured pursuant to an indenture trustee and designed to be bankruptcy remote, and advised the company on its $20.4M Series A funding round. She was recognized as a Finalist for the Corporate Counsel of the Year Award 2015 by LA Business Journal. She is the founder and co-organized of Legal Hackers LA, and was named one of the one of ten women to watch in legal technology by the American Bar Association Journal in 2014.