The new crowdfunding provisions in the “Jumpstart Our Business Startups Act of 2012” (which is often referred to as the “JOBS Act of 2012”) have received a lot of attention: Title III of the Act exempts certain crowdfundings from the registration requirements of the federal securities laws (the “Federal CF Exemption”), and the U. S. Securities and Exchange Commission issued proposed regulations in October 2013 to implement the exemption (the “Proposed CF Regulations”). The SEC received about 300 written comments to the Proposed CF Regulations, many of which related to the significant costs imposed by the proposed requirements. The SEC has not yet issued its final regulations despite a directive in the JOBS Act to do so by the end of 2012, and the Federal CF Exemption will not be effective until the SEC does so. A May 1, 2014 Wall Street Journal article, entitled “Frustration Rises Over Crowdfunding Rules,” describes efforts in the U.S. Congress to amend the JOBS Act even before the Federal CF Exemption takes effect. However, many states have found a way to go ahead with crowdfunding without the delay and burdens involved with the Federal CF Exemption. They have done so by adopting their own intrastate crowdfunding exemptions, often citing job creation as the goal.

The state crowdfunding exemptions cannot supersede the actions of the SEC, but there is a longstanding federal exemption from registration for intrastate offerings under Section 3(a)(11) of the Securities Act of 1933, as amended, and SEC Rule 147, which is a “safe harbor” means of compliance with Section 3(a)(11). States have generally written their new crowdfunding exemptions so that they work in tandem with the federal intrastate exemption. As explained below, this basically means that an issuer could be exempt at both the federal and state levels if it conducts an offering solely within the state in which it is organized and conducts its business. The state intrastate exemptions have generally removed certain of the more objectionable requirements of the Proposed CF Regulations, including use of a broker-dealer or “funding portal” for any exempt crowdfunding, preparation of audited financial statements for offerings of over $500,000 and distribution of periodic financial reports to investors after the offering. In addition, as described below, some of the exemptions have provided routes for raising amounts well beyond the $1 million cap under the Federal CF Exemption.

The state crowdfunding exemptions cannot supersede the actions of the SEC, but there is a longstanding federal exemption from registration for intrastate offerings under Section 3(a)(11) of the Securities Act of 1933, as amended, and SEC Rule 147, which is a “safe harbor” means of compliance with Section 3(a)(11). States have generally written their new crowdfunding exemptions so that they work in tandem with the federal intrastate exemption. As explained below, this basically means that an issuer could be exempt at both the federal and state levels if it conducts an offering solely within the state in which it is organized and conducts its business. The state intrastate exemptions have generally removed certain of the more objectionable requirements of the Proposed CF Regulations, including use of a broker-dealer or “funding portal” for any exempt crowdfunding, preparation of audited financial statements for offerings of over $500,000 and distribution of periodic financial reports to investors after the offering. In addition, as described below, some of the exemptions have provided routes for raising amounts well beyond the $1 million cap under the Federal CF Exemption.

Federal Intrastate Exemptions Not Too Popular

The federal intrastate exemption has not been very popular because most companies would find it easier to comply with other federal exemptions from registration, such as those provided by Regulation D. The intrastate offering exemption provides the opportunity for less burdensome crowdfunding for companies that can satisfy the federal intrastate requirements as well as the terms of any intrastate exemptions in their respective home states. Although Rule 147 is not the exclusive means of complying with the federal intrastate exemption, it is useful because it provides objective standards for compliance. Consistent with the single-state nature of the exemption, Rule 147 requires the issuer to be “resident and doing business” within the chosen state. A company can demonstrate residence by being organized and having its principal place of business in the state. (This may reduce the number of startups that are organized under Delaware law regardless of the locations of their businesses.)

Rule 147 is more challenging with respect to “doing business” within a particular state. The company must derive at least 80% of its gross revenues from the state, have at least 80% of its assets located in the state prior to any offering, use at least 80% of the net proceeds of the exempt offering to operate a business in the state and locate the principal office of the company in the state. Rule 147 also requires the company to offer and sell securities only to residents of the chosen state.

The single-state requirements of Rule 147 appear to be written by the economic development agency of a particular state: organize here, conduct most of your business here, use most of the offering proceeds here and locate your principal office here. However, because much of crowdfunding relates to local projects, the Rule 147 requirements are probably not too objectionable in most crowdfunding situations.

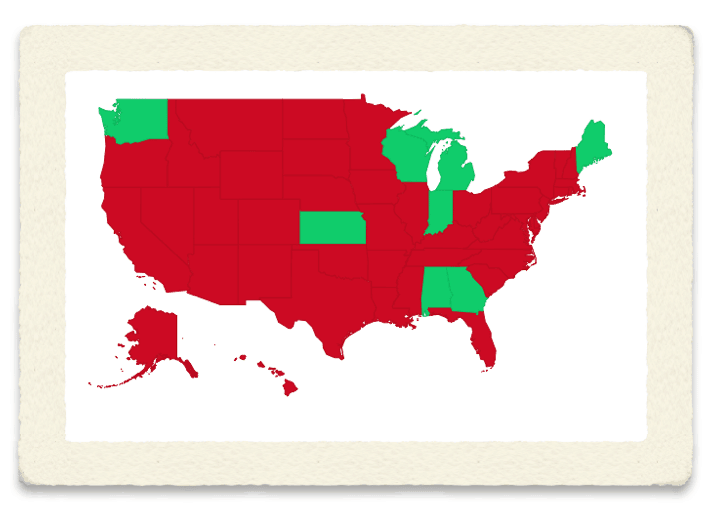

Kansas and Georgia were the first states to take advantage of the Rule 147 option with their “Invest Kansas Exemption” and “Invest Georgia Exemption,” respectively. Other states with intrastate exemptions from registration, as the result of legislative or regulatory action, include Alabama, Indiana, Michigan, Washington and Wisconsin. In addition, legislative or administrative action for a crowdfunding exemption is pending in Florida, New Jersey, North Carolina and Texas.

Kansas and Georgia were the first states to take advantage of the Rule 147 option with their “Invest Kansas Exemption” and “Invest Georgia Exemption,” respectively. Other states with intrastate exemptions from registration, as the result of legislative or regulatory action, include Alabama, Indiana, Michigan, Washington and Wisconsin. In addition, legislative or administrative action for a crowdfunding exemption is pending in Florida, New Jersey, North Carolina and Texas.

Most of the new state exemptions have the same offering cap as under the Federal CF Exemption–$1 million. However, some states increase the cap to $2 million if the issuer has audited financial statements (see, e.g., Indiana, Michigan, North Carolina and Wisconsin). The proposed New Jersey exemption could have a much higher offering cap. It provides for a limit of $1 million, but it excludes from the cap the amount sold to any “accredited investor” (generally, a natural person with annual income of over $200,000 or a net worth of over $1 million).

Investment Limitations

All of the state exemptions follow the federal principle that it is advisable to control potential losses by limiting the amount that may be invested by an individual investor. (It is worth noting, however, that there are no limits on the amounts that may be wagered in legalized gambling.) Under the Federal CF Exemption, the limitation on investment during a 12-month period depends on the income or net worth of the investor: the greater of $2,000 or 5% of annual income or net worth, if the annual income or net worth of the investor is under $100,000; and 10% of annual income or net worth (not to exceed an investment of $100,000), if the annual income or net worth of the investor is at least $100,000. The state exemptions have individual investment limitations ranging from $1,000 for Kansas to $10,000 for Georgia, Michigan and Wisconsin, irrespective of the income or net worth of the investor (except for the Washington exemption). Although no investor can invest over $100,000 under the Federal CF Exemption, the state exemptions generally permit an accredited investor to invest an unlimited amount (subject to the overall cap for the offering).

The Federal CF Exemption preempts state law in most respects, so once the SEC finalizes the regulations for the Federal CF Exemption, U.S. companies that comply with that exemption will be able to engage in crowdfunding in any state. However, they will not necessarily be able to use the cheaper and quicker intrastate crowdfunding exemptions that will be available only in those states that have adopted their own intrastate exemptions.

Will Intrastate Exemptions Boost State Economies?

The big unknown at this time is whether the availability of an intrastate crowdfunding exemption will bolster entrepreneurial activity in a particular state. There is already evidence that business groups in states that have intrastate exemptions may use them to recruit businesses from more restrictive states. A Georgia pro-business group has publicly invited Ohio entrepreneurs to move south where the capital-raising climate is friendlier.

The May 2013 issue of “Fast Company” magazine published a ranking of the “startup cultures” of the states and DC based on a number of factors (“The United States of Innovation”). Most people would probably expect California (i.e., Silicon Valley) to lead the list with Massachusetts (i.e., Boston) close behind. The top 10 list includes some surprises: 1. Florida, 2. Texas, 3. Maryland, 4. Arizona, 5. Alaska, 6. California, 8. New York, 9. New Jersey and 10. District of Columbia. Of these 10 jurisdictions, Florida, New Jersey and Texas have legislation or regulations pending to permit intrastate crowdfunding, but none of the others appears to have taken any action to permit the more liberal exemption.

Burdensome Requirements

Many commentators believe that the burdensome requirements of the Federal CF Exemption will defeat the JOBS-Act purpose of making it easier for small companies to raise capital, and as noted above, Congress is already proposing less costly amendments. The intrastate exemptions adopted by many states appear to provide a reasonable alternative for crowdfunding–an exemption that lacks certain expensive investor protections of the Federal CF Exemption, but that still limits the amount that individuals other than accredited investors could lose.

_______________________________

Tom Sharbaugh is a partner in the Business & Finance Practice Group of Morgan Lewis & Bockius LLP based in Philadelphia.

Tom Sharbaugh is a partner in the Business & Finance Practice Group of Morgan Lewis & Bockius LLP based in Philadelphia.