“The technology Orchard builds connects hundreds of millions of dollars of institutional capital to a rapidly expanding number of originators across multiple asset classes. This ultimately touches borrowers in an efficient and transparent manner, which truly makes what we do “many to many.”

Orchard has evolved organically from “what began as a small circle of friends with unique perspectives and complementary skill sets, driven by the same interests, and a desire to make a difference in the alternative lending space.” Working together as a team to build great products, serve our clients with excellence, and help shape the very nature of next-generation financial services is Orchard’s mission, a mission that has ignited significant and exciting success.

After swiftly raising $12 million in seed funding, Orchard has continued to be in the news. In recent weeks the platform announced two new partnerships as it extends its reach into a growing number of financial verticals in the direct lending space: Auto One Acceptance and The Interface Financial Group (IFG). In the last months, Orchard Platform also partnered with Kabbage and its consumer lending offshoot Karrot, Duff & Phelps and released its Orchard Manager Database described as a” comprehensive resource for institutional investors to identify and evaluate the funds of marketplace (P2P) lending investment managers.” Started in late 2011, Orchard Platform has clearly become one of the key leaders to watch in the Marketplace Lending sector, and one leader to watch is the platform’s Co-Founder and CFO Angela Ceresnie.

After swiftly raising $12 million in seed funding, Orchard has continued to be in the news. In recent weeks the platform announced two new partnerships as it extends its reach into a growing number of financial verticals in the direct lending space: Auto One Acceptance and The Interface Financial Group (IFG). In the last months, Orchard Platform also partnered with Kabbage and its consumer lending offshoot Karrot, Duff & Phelps and released its Orchard Manager Database described as a” comprehensive resource for institutional investors to identify and evaluate the funds of marketplace (P2P) lending investment managers.” Started in late 2011, Orchard Platform has clearly become one of the key leaders to watch in the Marketplace Lending sector, and one leader to watch is the platform’s Co-Founder and CFO Angela Ceresnie.

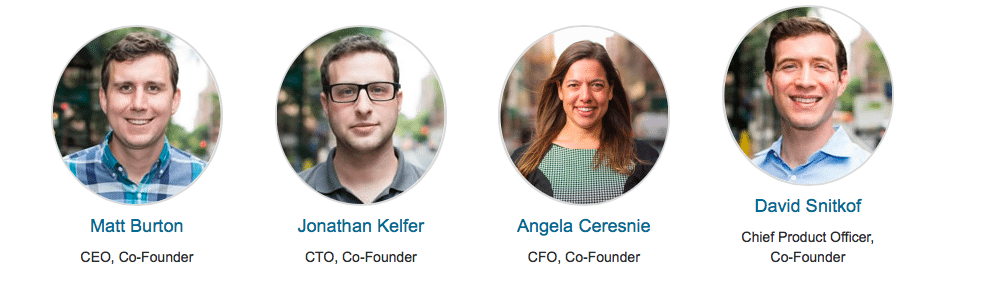

The Michigan grad began her career in Risk Management at American Express and Citibank before cofounding the institutional investment platform for the peer to peer, “many to many” and online direct lender with Matt Burton, Jonathan Kelfer and David Snitkof.

“Orchard does not originate loans and we do not touch borrowers. Orchard supports operational efficiencies to help institutional investors, investment managers and loan originators connect and transact,” commented Ceresnie in our interview. “While many of us have strong roots in traditional finance, Orchard has always been and will always be a technology-first company. We will always seek to build first-of-their kind products and to meet the needs of our customers to best enable them to participate in marketplace lending.”

In 2011 Burton lent $700 via Lending Club, a direct lending platform which links borrowers and creditors, according to The Economist: “He was pleased with his return of 8% until he discovered it was half that of Ceresnie who was working at the time in small-business lending at Citigroup. That prompted two insights: first, that there was money to be made by working with “originators”, meaning startups providing credit in novel ways; and second, that institutional investors would struggle to seize on this opportunity without an intermediary.”

Burton and Ceresnie ran the model, without any scraping, and then manually bought the individual loans, working their way up to around $100,000 in loans working 3 to 4 hours per week. Reaching back out to his Lending Club contacts, Burton gained access to some of the first API specs and plugged in directly to the source.

Burton and Ceresnie ran the model, without any scraping, and then manually bought the individual loans, working their way up to around $100,000 in loans working 3 to 4 hours per week. Reaching back out to his Lending Club contacts, Burton gained access to some of the first API specs and plugged in directly to the source.

I recently connected with financial maven Angela Ceresnie and learned more about her insight on several compelling topics, including her financial leadership, risk experience, Orchard’s founding, evolution and future. Our interview follows:

Erin: What prompted you to invest in Lending Club loans? What did you learn from that experience?

Angela: I discovered Lending Club in 2011 and was immediately attracted by three unique factors:

Angela: I discovered Lending Club in 2011 and was immediately attracted by three unique factors:

- They distribute 100% of their loans – taking no balance sheet risk

- Each loan is distributed at the loan level – enabling any type of investor to pick and choose what they want to invest in

- They make their historical loan book and performance publically available for investors to analyze

For the first time in modern banking history, I, a retail investor, was able to invest in a loan made directly to another person with full transparency into the borrower’s credit and financial data, the same data that was available to me in my current and past positions, running underwriting departments at banks.

Upon discovering this data, I followed my first instinct- to build a credit model and make some nice returns. I loved the diversity that this represented in my own personal portfolio, not to mention the yield. As I continued to research the new market, I realized how truly revolutionary it was.

Erin: How do/did you utilize your earlier credit risk analysis career experience at American Express and Citibank?

Angela: My background is in traditional finance. During the time I discovered Marketplace Lending, I was running the Small Business underwriting and analytics team at Citibank. Prior to that, I worked in consumer underwriting at American Express. Since moving to alternative finance, I have learned that you cannot de-legitimize the importance of experience: I was fortunate to have been given top notch training in terms of appreciating and understanding risk. In my initial personal participation in marketplace lending, I was able to take that knowledge and combine it with this interesting, newly available (to retail investors) data and build a model that I found to be superior.

Angela: My background is in traditional finance. During the time I discovered Marketplace Lending, I was running the Small Business underwriting and analytics team at Citibank. Prior to that, I worked in consumer underwriting at American Express. Since moving to alternative finance, I have learned that you cannot de-legitimize the importance of experience: I was fortunate to have been given top notch training in terms of appreciating and understanding risk. In my initial personal participation in marketplace lending, I was able to take that knowledge and combine it with this interesting, newly available (to retail investors) data and build a model that I found to be superior.

Erin: Describe that first P2P Meetup.

Angela: As soon as Matt, David, Jon and I got involved in marketplace lending, we knew we wanted to foster the disruptive and innovative nature of this space. Our goal was to create recurring events that could serve as an outlet for new ideas, concerns, thoughts and general camaraderie for individuals who shared the same excitement as we did, from this notion- the Meetup was born. We have since grown from our initial Meetups of a group of roughly 9 people meeting at Spitzer’s Corner in the Lower East Side using a paper sign in sheet to an international group comprised of 2,000 individuals. The venue has changed but the participants remain as hungry and spirited as ever.

Angela: As soon as Matt, David, Jon and I got involved in marketplace lending, we knew we wanted to foster the disruptive and innovative nature of this space. Our goal was to create recurring events that could serve as an outlet for new ideas, concerns, thoughts and general camaraderie for individuals who shared the same excitement as we did, from this notion- the Meetup was born. We have since grown from our initial Meetups of a group of roughly 9 people meeting at Spitzer’s Corner in the Lower East Side using a paper sign in sheet to an international group comprised of 2,000 individuals. The venue has changed but the participants remain as hungry and spirited as ever.

Erin: Middleware?

Angela: Our position in the marketplace came from the observation of a problem and the need for a solution: Institutions loved marketplace lending as an asset class but had no scalable system to use as a vehicle for participation. Our technology fills that gap.

Angela: Our position in the marketplace came from the observation of a problem and the need for a solution: Institutions loved marketplace lending as an asset class but had no scalable system to use as a vehicle for participation. Our technology fills that gap.

In the midst of consulting for institutions on Lending Club and Prosper, we realized that the big pain point would lie in the back office, or lack there of. We knew we needed to create something user friendly, cost effective, and most importantly scalable-—the first product launched shortly thereafter in early 2014. Because of the value we provide as an end-to-end solution, we don’t think of ourselves as middleware.

Erin: Orchard’s early clients were hedge funds, credit funds, alternative funds, banks, BDCs, family offices and wealth managers, but now include sizing up insurance companies, pensions and the entire panoply of institutional wealth. Who are your next targeted clients?

Angela: Our clients continue to be those named above. Our goal is to meet their needs as well as help both traditional and emerging originators scale their lending businesses.

Erin: How has Orchard created a “many to many” relationship using its technology?

Angela: The technology we build connects hundreds of millions of dollars of institutional capital to a rapidly expanding number of originators across multiple asset classes. This ultimately touches borrowers in an efficient and transparent manner, which truly makes what we do “many to many.”

Angela: The technology we build connects hundreds of millions of dollars of institutional capital to a rapidly expanding number of originators across multiple asset classes. This ultimately touches borrowers in an efficient and transparent manner, which truly makes what we do “many to many.”

Erin: How much revenue is Orchard generating? How many customers is Orchard currently servicing?

Angela: While we cannot disclose those details, we currently have between 50-99 clients capturing significant market share.

Erin: As an embracer of the financial ecosystem, please comment on the growing number of direct lending platform. Who do you see as peers and/or potential partners?

Erin: As an embracer of the financial ecosystem, please comment on the growing number of direct lending platform. Who do you see as peers and/or potential partners?

Angela: The marketplace lending ecosystem is certainly flourishing, that growth is readily seen in the constant development and increasing quality of origination platforms. Further, the amount of interest in this industry can be seen in the success of those high quality origination platforms. Origination platforms must be fundamentally good at 3 things in order to maintain quality borrowers for its investors. Those items include: acquiring borrowers, underwriting loans, and servicing those loans. Our platform is always looking to form relationships with originators who achieve those standards.

Erin: How will Orchard continue to build a system and maintain its origination platform that leverages today’s tech to build a better future?

Angela: To clarify, Orchard does not originate loans and we do not touch borrowers. Orchard supports operational efficiencies to help institutional investors, investment managers and loan originators connect and transact. While many of us have strong roots in traditional finance, Orchard has always been and will always be a technology-first company. We will always seek to build first-of-their kind products and to meet the needs of our customers to best enable them to participate in marketplace lending. What’s important to us is that we constantly add value, which is why we write our analytical blog and host frequent Marketplace Lending Meetups, always being sure to listen to the needs of our customers and partners in order to add the most possible value.

Erin: What are your thoughts on the next two or three years for marketplace lending? How and where will Orchard further expand? Where do you see Orchard in five years? ten years?

Angela: This is only the beginning for Marketplace Lending, this is the future of credit. Historically, the industrial revolution allowed us to standardize a process with computers and then repeat that process at scale. However, that opportunity came at the cost of personalization. For the first time in lending history, we have the ability to keep a specialized customer experience but do so at scale, and in a profitable way. We’ve all watched this happen in many different industries but now, the disruption is occurring in the world’s largest industry-finance.In terms of Orchard’s future, we want to be the platform that makes it easy and efficient for loans to be funded in a marketplace.

Erin: With your trailblazing experience as a fintech leader, what suggestions do you recommend both to close the gender gap in the investment management industry and to create gender balance in senior leadership positions?

Angela: In finance diversification is important when it comes to portfolio management. When it comes to the gender gap in the investment management industry, it’s the same thing. Every person brings different experiences and insights that are valuable to the bottom line. Diversify, Diversify, Diversify.

Angela: In finance diversification is important when it comes to portfolio management. When it comes to the gender gap in the investment management industry, it’s the same thing. Every person brings different experiences and insights that are valuable to the bottom line. Diversify, Diversify, Diversify.

Erin: Where have you witnessed effective efforts toward establishing equal gender representation at all career levels? How have women enabled, disrupted and innovated finance and fintech?

Angela: It’s part of the answer to the last question and I’ve seen this first hand with my co-founders. Every person brings an expertise to the table and the more diversified the team, the more successful they will ultimately be. Women bring a different perspective to the table. It really is about striking a balance and creating an environment where everyone can draw upon their experience and is set up for success. The success of a company ultimately reflects that.

Erin: Please share your P2P and credit risk mentors. Who have you mentored to create financial change and innovation?

Angela: Jerry Weis formerly of CitiBank and now of Bond Street, and Tina Reich formerly of CitiBank and American Express, now at Retail Capital. These are people who taught me the principles of assessing and managing credit and general management principles. My management style is all about feedback, honesty and openness. Transparent leadership and being clear about values and expectations are the most important things when it comes to management, those characteristics enable everyone to be effective- many of these skills I learned from Jerry and Tina.

Erin: Early investors in Orchard include Doug Atkin of Guggenheim Partners, Jennifer Hyman, CEO, Co-Founder Rent the Runway, Vikram Pandit (former chief executive at Citigroup) and Tom Glocer (former CEO of Thomson Reuters). How did these investors influence the platform? How are they still involved with Orchard?

Erin: Early investors in Orchard include Doug Atkin of Guggenheim Partners, Jennifer Hyman, CEO, Co-Founder Rent the Runway, Vikram Pandit (former chief executive at Citigroup) and Tom Glocer (former CEO of Thomson Reuters). How did these investors influence the platform? How are they still involved with Orchard?

Angela: Each investor adds unique value and insights, and we’re grateful for their believing in us early on.

Erin: As Orchard moves fintech forward, what kinds of tools are needed to help “institutional investors deploy capital efficiently and origination platforms operate a marketplace for selling their loans?” How are Orchard’s analytics and automated investment platform evolving?

Angela: Institutional Investors and managers work with Orchard to deploy capital in the sector in an effective, efficient, and data-driven manner. Tools that enable them to do this include the Originator Database, the Manager Database, custom portfolio reporting & analytics, and an order management system to acquire loans across multiple different originators. Originators use Orchard to diversify their capital structure and more efficiently distribute their debt, through full integration (available for both offline and online lenders) and Originator Database participation.

This is part of a series of articles where Crowdfund Insider will be interviewing the many women changing the profession of finance today. In FinTech, crowdfunding and peer to peer lending, there are many female entrepreneurs leading or assisting innovative firms that are altering the process of capital formation around the globe.

This is part of a series of articles where Crowdfund Insider will be interviewing the many women changing the profession of finance today. In FinTech, crowdfunding and peer to peer lending, there are many female entrepreneurs leading or assisting innovative firms that are altering the process of capital formation around the globe.