2015 could go down as the most active year for regulatory reform in the private securities market since 1940. After a long delay since passage of the JOBS Act in 2012, we saw an unprecedented flurry of regulatory activity in 2015.

Without further ado, here are the top 10 crowdfunding and private securities legal developments of 2015:

#10 – RAISE Act and Private Secondary Markets (December 2015).

Snuck into a transportation bill, the Reforming Access for Investments in Startup Enterprises (“RAISE”) Act formalizes a securities exemption for shareholders to sell their shares on a secondary market. In short, employees and early shareholders can now rely on a statute to sell their shares in private companies to accredited investors so long as they meet certain conditions. Prior to the RAISE Act, most sellers relied on an informal exemption developed under case law, referred to as the 4(a)1/2 exemption and which has now been codified into 4(a)(7). The typical case here is the startup employee who desires to sell his shares before the company is sold or goes public. These type of secondary sales have been popularized by companies like SecondMarket and EquityZen.

Snuck into a transportation bill, the Reforming Access for Investments in Startup Enterprises (“RAISE”) Act formalizes a securities exemption for shareholders to sell their shares on a secondary market. In short, employees and early shareholders can now rely on a statute to sell their shares in private companies to accredited investors so long as they meet certain conditions. Prior to the RAISE Act, most sellers relied on an informal exemption developed under case law, referred to as the 4(a)1/2 exemption and which has now been codified into 4(a)(7). The typical case here is the startup employee who desires to sell his shares before the company is sold or goes public. These type of secondary sales have been popularized by companies like SecondMarket and EquityZen.

Upshot: This is a step in the right direction for facilitating secondary markets and liquidity for private securities.

#9 – Accredited Investor Definition – SEC Staff Recommendations (December 2015).

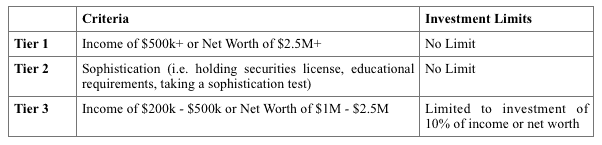

This may have the most dramatic impact across the securities markets. Regulation D offerings to accredited investors account for nearly all current fundraising for private companies and private funds. Some have proposed changes to the accredited investor definition that could seriously hamper startup and small business fundraising by reducing the number of accredited investors in the country by over 50%.

In response to this possibility, there was an avalanche of feedback delivered to the SEC, advocating to; (1) leave the financial thresholds alone (if it ain’t broke…) and, (2) potentially expand the definition to include certain sophisticated persons.

In December of this year, the SEC staff released its recommendations, which effectively created 3 “tiers” of Accredited Investors:

*All numbers would be indexed to inflation going forward.

Upshot: Disaster seems to be averted and there may even be a new class of sophisticated millennial/young professional accredited investors. On the downside, transactions would have moderately more friction and legal expense. There is still some work to be done here, in particular on clarifying the proposed sophistication standards under Tier 2, but all-in-all a positive result for fundraising. These recommendations are out for comment are not final.

#8 – CitizenVC No Action Letter (August 2015).

In this letter, the Securities and Exchange Commission confirmed that an online investment platform can operate under Rule 506(b) of Regulation D without being deemed to have engaged in General Solicitation so long as proper procedures are followed. While the letter did not contain any surprises, it dispelled many incorrect interpretations of the law prevailing in the market and also provided more certainty to those seeking to operate under Rule 506(b). In pertinent part, the letter dismissed the idea that a 30 day cooling off period is mandatory for platforms operating under Rule 506(b).

Upshot: Many investment platforms are now pulling back to conducting “private” Rule 506(b) offerings rather than “public” Rule 506(c) offerings.

#7 – Regulation A+ Implemented (June 2015).

On June 19, 2015, Title IV of the JOBS Act went into effect allowing companies to raise up to $50M in a “mini-IPO” style offering. On the first day, several offerings launched into “testing the waters” and received a strong response. Subsequently, the Elio Motors offering was qualified by the SEC on November 20, 2015, and the fundraising is currently underway.

Upshot: The verdict is still out on the effectiveness of straight Regulation A+ offerings. If costs are contained and these companies are successful in raising significant amounts of money, then a new alternative to venture capital and private equity capital could emerge for mid-sized businesses.

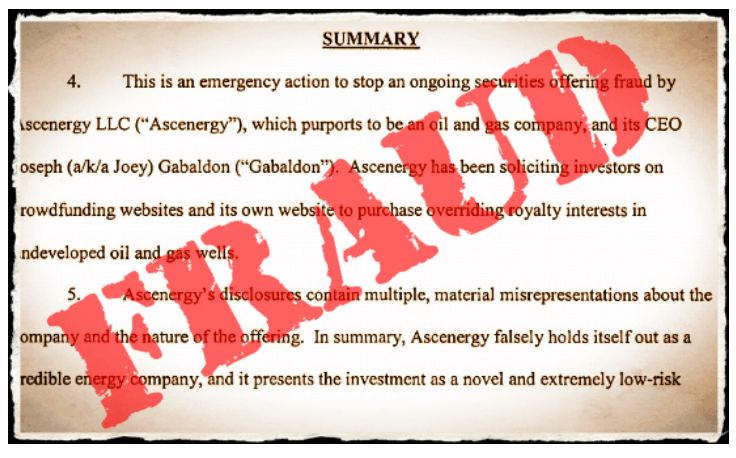

#6 – SEC Action against Ascenergy Oil & Gas Crowdfunding Scheme (October 2015).

The SEC has been active on the enforcement front. In this case, Ascenergy raised $5M from over 90 investors including via listings on several funding platforms for oil & gas projects. The SEC found that most of the proceeds were actually being used for other purposes including payments to the principals and not oil and gas development. Notably, Ascenergy did not appear on any platform operated by a broker-dealer, but rather listed on the more “open” non-broker dealer platforms.

The SEC has been active on the enforcement front. In this case, Ascenergy raised $5M from over 90 investors including via listings on several funding platforms for oil & gas projects. The SEC found that most of the proceeds were actually being used for other purposes including payments to the principals and not oil and gas development. Notably, Ascenergy did not appear on any platform operated by a broker-dealer, but rather listed on the more “open” non-broker dealer platforms.

Upshot: In the wake of sweeping regulatory change, regulators are on high alert for fraud and bad actors and are willing to take action.

#5 – PATH Act Permanently Extends QSBS Tax Exclusion (December 2015).

In a big win for angel investors, the PATH Act makes permanent a 100% capital gains tax exclusion for “qualified small business stock.” In short, if an individual purchases shares in a qualified small business (i.e. a startup) and holds it for 5 years, they will not be required to pay taxes on the gain on those shares, subject to several conditions. Historically, the Angel Capital Association and others have been fighting for annual extensions for this exclusion, which is now permanent.

In a big win for angel investors, the PATH Act makes permanent a 100% capital gains tax exclusion for “qualified small business stock.” In short, if an individual purchases shares in a qualified small business (i.e. a startup) and holds it for 5 years, they will not be required to pay taxes on the gain on those shares, subject to several conditions. Historically, the Angel Capital Association and others have been fighting for annual extensions for this exclusion, which is now permanent.

Upshot: Qualified small businesses that are raising capital should make sure their investors are aware of this potentially large tax benefit.

#4 – Intrastate Crowdfunding – Modernization of Rule 147 and Rule 504 (October 2015).

During the wait for the Title III Equity Crowdfunding rules, over 30 states took matters into their own hands and implemented intrastate crowdfunding rules. Usage of these laws has been low and many view the uncertainty created by the interaction with federal law as the primary culprit. Now the SEC has proposed to fix the federal rules to pave the way for intrastate crowdfunding by, among other things (i) allowing internet advertising, (ii) allowing companies incorporated in other states (i.e. Delaware) to participate, and (iii) providing more flexibility on how to qualify as doing business in a particular state (i.e. if a majority of your employees are in the state, then the company can qualify as doing business in that state).

Upshot: State crowdfunding laws, which are generally much less stringent than national crowdfunding under Title III of the JOBS Act, could provide a useful path for local crowdfunding.

#3- Overstock Gets SEC Approval to Issue Shares Using Blockchain (Dec 2015).

In the latest proposal to use blockchain technology to disrupt existing industries, Overstock is seeking to create a new, digital, securities market where we are no longer reliant on broker-dealers and other intermediaries. In theory, such a system could replace existing trading markets (i.e. the NYSE, NASDAQ and OTC) and eliminate bid/ask spreads.

In the latest proposal to use blockchain technology to disrupt existing industries, Overstock is seeking to create a new, digital, securities market where we are no longer reliant on broker-dealers and other intermediaries. In theory, such a system could replace existing trading markets (i.e. the NYSE, NASDAQ and OTC) and eliminate bid/ask spreads.

Upshot: This is likely the first of many concepts where the blockchain is applied to the securities markets.

#2 – SEC qualifies Fundrise Reg A+ “eREIT” (November 2015).

Unlike Regulation Crowdfunding, the Regulation A+ rules are not specifically restricted to operating companies, opening the door for certain types of investment vehicles (so long as they also comply with other applicable regulation). Ultimately, this could be the most powerful use case for Regulation A+. The eREIT allows Fundrise to accept investments from unaccredited investors and deploy them across a variety of real estate investment asset classes.

Unlike Regulation Crowdfunding, the Regulation A+ rules are not specifically restricted to operating companies, opening the door for certain types of investment vehicles (so long as they also comply with other applicable regulation). Ultimately, this could be the most powerful use case for Regulation A+. The eREIT allows Fundrise to accept investments from unaccredited investors and deploy them across a variety of real estate investment asset classes.

Upshot: This is a huge development in the real estate crowdfunding market as well as for the massive traditional REIT market. We expect to see many more Reg A+ REIT filings from platforms and traditional REIT managers in 2016.

#1 – Title III Equity Crowdfunding Final Rules (October 2015).

The wait is finally coming to an end and we will have legal, national, securities crowdfunding rules effective on May 16, 2016. These rules provide a framework for raising capital up to $1M from both unaccredited and accredited investors subject to a plethora of requirements, restrictions, regulations, and limitations. While many have written Title III crowdfunding off as too complicated, burdensome, expensive or regulated, many platforms are eagerly pressing forward with plans to launch equity crowdfunding offerings this summer.

The wait is finally coming to an end and we will have legal, national, securities crowdfunding rules effective on May 16, 2016. These rules provide a framework for raising capital up to $1M from both unaccredited and accredited investors subject to a plethora of requirements, restrictions, regulations, and limitations. While many have written Title III crowdfunding off as too complicated, burdensome, expensive or regulated, many platforms are eagerly pressing forward with plans to launch equity crowdfunding offerings this summer.

Upshot: As many of the established players are shying away from Title III crowdfunding, those platforms that are able to figure out how to navigate and automate the regulatory requirements and transaction processes in a cost effective manner could be well positioned to dominate this market for many years to come.

2016 – The Year of Opportunity

Bonus – Reg A+ Shelf Registration. In Q1 2016, we could see the first approved Regulation A+ shelf registration, which would allow deal-by-deal access to unaccredited investors through a borrower payment dependent note structure. This would be similar to how Lending Club and Prosper reach unaccredited investors, but with the lower costs and compliance obligations of a Regulation A+ offering (as compared to a full-fledged IPO). For debt offerings, this could prove to be more effective than Title III crowdfunding.

Bonus – Reg A+ Shelf Registration. In Q1 2016, we could see the first approved Regulation A+ shelf registration, which would allow deal-by-deal access to unaccredited investors through a borrower payment dependent note structure. This would be similar to how Lending Club and Prosper reach unaccredited investors, but with the lower costs and compliance obligations of a Regulation A+ offering (as compared to a full-fledged IPO). For debt offerings, this could prove to be more effective than Title III crowdfunding.

While 2015 brought us sweeping regulatory changes, 2016 may be the year where we see rapid innovation as industry leaders identify new market opportunities created by these developments.

Kiran Lingam is a Partner in FinTech at Nelson Mullins Riley and Scarborough and Managing Director of LendTech Angels. He has written several of the seminal articles on new securities laws under the JOBS Act, including on Accredited Investor Crowdfunding (Title II), Retail Crowdfunding (Title III) and Regulation A (Title IV). Prior to Nelson Mullins, Kiran was General Counsel at equity crowdfunding platform SeedInvest. He is a Charter Member and Board member of TiE (The Indus Entrepreneurs) and TiE Angels. Kiran received a B.A. in Economics from Cornell University and a J.D., with honors, from the University of Georgia.

Kiran Lingam is a Partner in FinTech at Nelson Mullins Riley and Scarborough and Managing Director of LendTech Angels. He has written several of the seminal articles on new securities laws under the JOBS Act, including on Accredited Investor Crowdfunding (Title II), Retail Crowdfunding (Title III) and Regulation A (Title IV). Prior to Nelson Mullins, Kiran was General Counsel at equity crowdfunding platform SeedInvest. He is a Charter Member and Board member of TiE (The Indus Entrepreneurs) and TiE Angels. Kiran received a B.A. in Economics from Cornell University and a J.D., with honors, from the University of Georgia.